QTA Rueckkauf 0,08

Dax © 24.290 -0,33%

Dow Jones 44.326 0

S&P 500 6.297 -0,01%

Dow Jones 44.326 0

S&P 500 6.297 -0,01%

Nasdaq 23.055 +0,00%

Nikkei 39.690 +0,00%

Hang Seng 24.826 +1,33%

Nikkei 39.690 +0,00%

Hang Seng 24.826 +1,33%

EUR/USD 1,16259 +0,27%

BTC/USD 118.332 +0,28%

ETH/USD 3.564 +0,44%

BTC/USD 118.332 +0,28%

ETH/USD 3.564 +0,44%

App installieren

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Anmerkung: This feature may not be available in some browsers.

Du verwendest einen veralteten Browser. Es ist möglich, dass diese oder andere Websites nicht korrekt angezeigt werden.

Du solltest ein Upgrade durchführen oder einen alternativen Browser verwenden.

Du solltest ein Upgrade durchführen oder einen alternativen Browser verwenden.

Rohstoffthread / CCG-Hauptthread

- Ersteller dukezero

- Erstellt am

- Tagged users Kein(e)

Ganz übel - FM

sollte eigentlich besser dastehen, bisher sehr solide aufgebaut.

IRW-News: Inca One Gold Corp.: INCA ONE engagiert Jett Capital Advisors zur Beschaffung von Geldmitteln in Höhe von bis zu 20 Mio. USD für Betriebserweiterung

http://www.finanzen.net/nachricht/aktien/IRW-News-Inca-One-Gold-Corp-INCA-ONE-engagiert-Jett-Capital-Advisors-zur-Beschaffung-von-Geldmitteln-in-Hoehe-von-bis-zu-20-Mio-USD-fuer-Betriebserweiterung-4535097

IRW-News: Inca One Gold Corp.: INCA ONE engagiert Jett Capital Advisors zur Beschaffung von Geldmitteln in Höhe von bis zu 20 Mio. USD für Betriebserweiterung

http://www.finanzen.net/nachricht/aktien/IRW-News-Inca-One-Gold-Corp-INCA-ONE-engagiert-Jett-Capital-Advisors-zur-Beschaffung-von-Geldmitteln-in-Hoehe-von-bis-zu-20-Mio-USD-fuer-Betriebserweiterung-4535097

Und trotz des Absturzes ist FM noch kein fundamentaler Kauf, wenn dann nur ein riskanter Zock:

Announcement: Moody's: FQM's outlook remains negative despite $1.1 billion cash injection

London, 28 September 2015 -- Moody's Investors Service, ("Moody's") has today downgraded by one notch the corporate family rating (CFR) and the probability of default rating (PDR) of First Quantum Minerals Ltd (FQM) to B2 and B2-PD, respectively. Concurrently, the rating agency has downgraded the ratings on all of the senior unsecured notes issued by FQM to B3 from B2. The outlook on all ratings is negative.

"Our downgrade of First Quantum Minerals to B2 reflects the deterioration in the company's financial profile and our expectation that their credit metrics are unlikely to realign by the end of 2016 to levels commensurate with a B1 rating, particularly with continuing concerns over the knock on impact of lower copper and nickel prices, which are unlikely to change, on the business", said Douglas Rowlings, Moody's Analyst and local market analyst for FQM.

RATINGS RATIONALE

Under the rating agency's revised base metal price assumptions and factoring in FQM's locked in prices for production, Moody's does not expect that these credit metrics will realign with a B1 rating by the end of 2016. On 10 September 2015, Moody's revised its 2016 base price assumptions for copper to $2.35/lb from $3/lb and nickel to $4.8/lb from $6.25/lb. Capital expenditure at FQM's Cobre Panama project will continue to weigh on free cash flow generation and FQM's ability to reduce debt levels.

At the same time the B2 CFR also factors in the material production exposure that FQM has to Zambia through its mines in the country. Moody's downgraded Zambia to B2 with a stable outlook, from B1 with a negative outlook on 25 September 2015. Moody's is unlikely to rate FQM higher than Zambia's sovereign rating, for now, because of its heavy reliance on mining operations in the country and the strong link between operating performance and government policy. FQM's two Zambian mines, Kansanshi and Sentinel, are expected to generate in the region of 50% of total cash flow until the Cobre Panama mine in Panama (Baa2 stable) reaches full production levels in 2018.

Despite these challenges, FQM's credit profile continues to benefit from a number of operational risk mitigants. The company has a natural hedge against a low copper price through its low C1 cash cost that Moody's expects will be close to lower end of 2015 guidance of $1.25-1.4/lb, which compares favorably with its copper mining peers on the global industry cost curve with an average of around $1.5/lb. The company also has a strong demonstrated track record of finding buyers for the production it supplies to the market. The Zambian government has already implemented a number of proactive measures to shore up electricity, which include adding power from alternative sources, along with accelerating start dates for new power generation capacity. This will add to grid supply and electricity distribution to FQM's Kansanshi and Sentinel mines.

RATIONALE FOR THE NEGATIVE OUTLOOK

The negative outlook factors in the near-term challenges that the FQM's credit profile will continue to face. These include (1) continued electricity supply uncertainty in Zambia and the impact on FQM's production levels and costs should electricity tariffs increase; (2) a weak base metal price environment where under Moody's stress price assessment of a copper price at $2.2/lb and a nickel price of $4.4/lb, FQM's B2 rating would come under pressure; and (3) uncertainty surrounding the ability to meet the 4.5x net debt/EBITDA bank covenant target in second half of 2016, where Moody's assessment of FQM's ability to meet funding needs remains reliant upon availability under its $3 billion senior revolving credit facility.

A stable outlook could be considered once there is greater certainty around (1) FQM's ability to prospectively meet bank facility covenants in the second half of 2016; (2) sufficient electricity supply to both Kansanshi and Sentinel mines in Zambia with no meaningful impact on costs if electricity tariffs were to be increased; and (3) realignment of operations and capital expenditure spend to protect against a volatile low copper and nickel price environment.

WHAT COULD CHANGE THE RATING -- UP/DOWN

FQM's rating could be downgraded to B3 if it appeared likely that the debt to EBITDA ratio above 5x and EBIT to interest ratio below 2x would be sustained over the next 12 to 18 months and should liquidity contract.

An upgrade to FQM's ratings is unlikely until such time that there material production diversification away from Zambia (B2 stable), given the linkage of operation performance operating risk profile in the country and Zambia's government policy.

The principal methodology used in these ratings was Global Mining Industry published in August 2014. Please see the Credit Policy page on www.moodys.com for a copy of these methodology.

First Quantum Minerals Ltd (FQM), headquartered in Canada and listed on the Toronto Stock Exchange and the London Stock Exchange, is a medium size mining company with a large operation in Zambia (B2 stable), where it manages Kansanshi, a large and low-cost copper and gold deposit. FQM also operates a small copper and gold mine in Mauritania (unrated), a nickel mine in Australia (Aaa stable), a copper-nickel and copper-zinc mine in Finland (Aaa negative), a copper mine in Spain (Baa2 positive) and another one in Turkey (Baa3 negative). FQM has an 80% interest in Cobre Panama one of the world's largest copper deposits in Panama (Baa2 stable). For the last 12 months ended 30 June 2015 FQM reported revenues of $2.966 billion and EBITDA of $998.8 million.

The Local Market analyst for this rating is Douglas Rowlings, 971.4.237.9543.

REGULATORY DISCLOSURES

Announcement: Moody's: FQM's outlook remains negative despite $1.1 billion cash injection

London, 28 September 2015 -- Moody's Investors Service, ("Moody's") has today downgraded by one notch the corporate family rating (CFR) and the probability of default rating (PDR) of First Quantum Minerals Ltd (FQM) to B2 and B2-PD, respectively. Concurrently, the rating agency has downgraded the ratings on all of the senior unsecured notes issued by FQM to B3 from B2. The outlook on all ratings is negative.

"Our downgrade of First Quantum Minerals to B2 reflects the deterioration in the company's financial profile and our expectation that their credit metrics are unlikely to realign by the end of 2016 to levels commensurate with a B1 rating, particularly with continuing concerns over the knock on impact of lower copper and nickel prices, which are unlikely to change, on the business", said Douglas Rowlings, Moody's Analyst and local market analyst for FQM.

RATINGS RATIONALE

Under the rating agency's revised base metal price assumptions and factoring in FQM's locked in prices for production, Moody's does not expect that these credit metrics will realign with a B1 rating by the end of 2016. On 10 September 2015, Moody's revised its 2016 base price assumptions for copper to $2.35/lb from $3/lb and nickel to $4.8/lb from $6.25/lb. Capital expenditure at FQM's Cobre Panama project will continue to weigh on free cash flow generation and FQM's ability to reduce debt levels.

At the same time the B2 CFR also factors in the material production exposure that FQM has to Zambia through its mines in the country. Moody's downgraded Zambia to B2 with a stable outlook, from B1 with a negative outlook on 25 September 2015. Moody's is unlikely to rate FQM higher than Zambia's sovereign rating, for now, because of its heavy reliance on mining operations in the country and the strong link between operating performance and government policy. FQM's two Zambian mines, Kansanshi and Sentinel, are expected to generate in the region of 50% of total cash flow until the Cobre Panama mine in Panama (Baa2 stable) reaches full production levels in 2018.

Despite these challenges, FQM's credit profile continues to benefit from a number of operational risk mitigants. The company has a natural hedge against a low copper price through its low C1 cash cost that Moody's expects will be close to lower end of 2015 guidance of $1.25-1.4/lb, which compares favorably with its copper mining peers on the global industry cost curve with an average of around $1.5/lb. The company also has a strong demonstrated track record of finding buyers for the production it supplies to the market. The Zambian government has already implemented a number of proactive measures to shore up electricity, which include adding power from alternative sources, along with accelerating start dates for new power generation capacity. This will add to grid supply and electricity distribution to FQM's Kansanshi and Sentinel mines.

RATIONALE FOR THE NEGATIVE OUTLOOK

The negative outlook factors in the near-term challenges that the FQM's credit profile will continue to face. These include (1) continued electricity supply uncertainty in Zambia and the impact on FQM's production levels and costs should electricity tariffs increase; (2) a weak base metal price environment where under Moody's stress price assessment of a copper price at $2.2/lb and a nickel price of $4.4/lb, FQM's B2 rating would come under pressure; and (3) uncertainty surrounding the ability to meet the 4.5x net debt/EBITDA bank covenant target in second half of 2016, where Moody's assessment of FQM's ability to meet funding needs remains reliant upon availability under its $3 billion senior revolving credit facility.

A stable outlook could be considered once there is greater certainty around (1) FQM's ability to prospectively meet bank facility covenants in the second half of 2016; (2) sufficient electricity supply to both Kansanshi and Sentinel mines in Zambia with no meaningful impact on costs if electricity tariffs were to be increased; and (3) realignment of operations and capital expenditure spend to protect against a volatile low copper and nickel price environment.

WHAT COULD CHANGE THE RATING -- UP/DOWN

FQM's rating could be downgraded to B3 if it appeared likely that the debt to EBITDA ratio above 5x and EBIT to interest ratio below 2x would be sustained over the next 12 to 18 months and should liquidity contract.

An upgrade to FQM's ratings is unlikely until such time that there material production diversification away from Zambia (B2 stable), given the linkage of operation performance operating risk profile in the country and Zambia's government policy.

The principal methodology used in these ratings was Global Mining Industry published in August 2014. Please see the Credit Policy page on www.moodys.com for a copy of these methodology.

First Quantum Minerals Ltd (FQM), headquartered in Canada and listed on the Toronto Stock Exchange and the London Stock Exchange, is a medium size mining company with a large operation in Zambia (B2 stable), where it manages Kansanshi, a large and low-cost copper and gold deposit. FQM also operates a small copper and gold mine in Mauritania (unrated), a nickel mine in Australia (Aaa stable), a copper-nickel and copper-zinc mine in Finland (Aaa negative), a copper mine in Spain (Baa2 positive) and another one in Turkey (Baa3 negative). FQM has an 80% interest in Cobre Panama one of the world's largest copper deposits in Panama (Baa2 stable). For the last 12 months ended 30 June 2015 FQM reported revenues of $2.966 billion and EBITDA of $998.8 million.

The Local Market analyst for this rating is Douglas Rowlings, 971.4.237.9543.

REGULATORY DISCLOSURES

[url=http://peketec.de/trading/viewtopic.php?p=1627823#1627823 schrieb:

Kostolanys Erbe

RohstoffExperte

Ort:

Im schönsten Bundesland zwischen Nord- und Ostsee.

Beiträge:

11.152

Trades:

4

Da bin ich persönlich anderer Meinung.

Ich sehe bei IO nur Schulden und dann evtl. bald neue Schulden die dazu kommen!

Ich sehe bei IO nur Schulden und dann evtl. bald neue Schulden die dazu kommen!

[url=http://peketec.de/trading/viewtopic.php?p=1627830#1627830 schrieb:Rookie schrieb am 28.09.2015, 18:31 Uhr[/url]"]sollte eigentlich besser dastehen, bisher sehr solide aufgebaut.

IRW-News: Inca One Gold Corp.: INCA ONE engagiert Jett Capital Advisors zur Beschaffung von Geldmitteln in Höhe von bis zu 20 Mio. USD für Betriebserweiterung

http://www.finanzen.net/nachricht/aktien/IRW-News-Inca-One-Gold-Corp-INCA-ONE-engagiert-Jett-Capital-Advisors-zur-Beschaffung-von-Geldmitteln-in-Hoehe-von-bis-zu-20-Mio-USD-fuer-Betriebserweiterung-4535097

Mit den Schulden hast Du nicht ganz unrecht, aber die Anlage und das zu verarbeitende Material mussten erstmal finanziert werden.

Es muss unbedingt die Grossmarge verbessert werden, das haben sie jetzt durch den Ankauf der Desorptionsanlage verbessert. Auch die Ausbringung und die Qualität des Ankaufmaterials werden sie erhöhen.

Ohne Ausweitung der Verarbeitung können sie nicht die OPEX abdecken.

Gross Marge 131.142 CAD, OPEX 3,6 Mill. CAD.

Darum stehen sie im Kurs momentan dort.

Bisher wurden sie von einer Schweizer Gruppe finanziert, die letzte Finanzierung lief als Gypsy swap ab.

Aber vielleicht habe ich etwas übersehen, bin immer an anderen Meinungen interessiert.

Es muss unbedingt die Grossmarge verbessert werden, das haben sie jetzt durch den Ankauf der Desorptionsanlage verbessert. Auch die Ausbringung und die Qualität des Ankaufmaterials werden sie erhöhen.

Ohne Ausweitung der Verarbeitung können sie nicht die OPEX abdecken.

Gross Marge 131.142 CAD, OPEX 3,6 Mill. CAD.

Darum stehen sie im Kurs momentan dort.

Bisher wurden sie von einer Schweizer Gruppe finanziert, die letzte Finanzierung lief als Gypsy swap ab.

Aber vielleicht habe ich etwas übersehen, bin immer an anderen Meinungen interessiert.

[url=http://peketec.de/trading/viewtopic.php?p=1627882#1627882 schrieb:Kostolanys Erbe schrieb am 28.09.2015, 22:44 Uhr[/url]"]Da bin ich persönlich anderer Meinung.

Ich sehe bei IO nur Schulden und dann evtl. bald neue Schulden die dazu kommen!

[url=http://peketec.de/trading/viewtopic.php?p=1627830#1627830 schrieb:Rookie schrieb am 28.09.2015, 18:31 Uhr[/url]"]sollte eigentlich besser dastehen, bisher sehr solide aufgebaut.

IRW-News: Inca One Gold Corp.: INCA ONE engagiert Jett Capital Advisors zur Beschaffung von Geldmitteln in Höhe von bis zu 20 Mio. USD für Betriebserweiterung

http://www.finanzen.net/nachricht/aktien/IRW-News-Inca-One-Gold-Corp-INCA-ONE-engagiert-Jett-Capital-Advisors-zur-Beschaffung-von-Geldmitteln-in-Hoehe-von-bis-zu-20-Mio-USD-fuer-Betriebserweiterung-4535097

Vielleicht sehen wir jetzt nochmals einen Ausverkauf den wir uns nicht vorgestellt haben.

Allerdings sind ja viele kleinere Unternehmen schon nahe Null.....naja,Galgenhumor

Guten Morgen. Schon länger nicht hier gewesen.

Sehe das mit den Schulden ähnlich, da werden einige platt gemacht, so scheint es zumindest, zu hohe Produktionskosten, aber irgendwann sollte doch das Angebot dann ziemlich abreißen und für steigende Rohstoffpreise sorgen. Oder wird aktuell soviel über-produziert?

Mein Long Wert Alkane Resources halte ich nach wie vor für aussichtsreich,

bei aktuellen Rohstoffpreisen gab es folgende financial study, nicht unerwähnt bleiben sollte das alle Genehmigungen für das Projekt erteilt wurden, und Alkane seit über 8 Jahren eine Demo-Anlage für die Separation betreibt, welche sie stetig verbessert haben .. das können meines Erachtens wenige Explorer/Produzenten vorweisen ..

29.09.2015 Alkane Resources (ASX:ALK) has signed an agreement with global minerals and metals processing technology supplier Outotec to conduct an Early Contractor Involvement process for the Dubbo Zirconia Project (DZP) in New South Wales.

This is a key step in development of the project and will aid compilation of the financing package. DZP is expected to generate annual revenue of $580 million delivering EBITDA of $320 million and a 20-year NPV of $1.22 billion.

.....

Discussions on the financing are advancing and are run in parallel and in conjunction with completing product off-take agreements.

Alkane remains well-funded with A$14.8 million in cash at the end of June 2015, along with A$4.8 million in bullion and no debt.

Aktuelle MCAP 100 Mio A$. Bei aktuellen Goldpreisen von 1600 A$ und Produktionskosten von ~1200A$ und Produktion von 60-70000oz bleiben hier 20 Mio über, keine Schulden, die aktuellen Überschüsse aus dem Goldprojekt fließen in die Entwicklung des DZP Projekts, interessant wird hier die Finanzierung von 1,3 Mrd welche für das Projekt notwendig ist, aber über staatliche Mittel, oder einen Teilverkauf (10-20%) des Projekts finanziert werden soll, eine KE soll erst bei deutlich höheren Kursen durchgefüht werden, .. ich finde es spannend. Aktuell allerdings fast kein Handel, selbst in AUS gehen nur 50-300.000 Stk um ..

Viel Erfolg, werde hier mal wieder mehr mitlesen 8)

Sehe das mit den Schulden ähnlich, da werden einige platt gemacht, so scheint es zumindest, zu hohe Produktionskosten, aber irgendwann sollte doch das Angebot dann ziemlich abreißen und für steigende Rohstoffpreise sorgen. Oder wird aktuell soviel über-produziert?

Mein Long Wert Alkane Resources halte ich nach wie vor für aussichtsreich,

bei aktuellen Rohstoffpreisen gab es folgende financial study, nicht unerwähnt bleiben sollte das alle Genehmigungen für das Projekt erteilt wurden, und Alkane seit über 8 Jahren eine Demo-Anlage für die Separation betreibt, welche sie stetig verbessert haben .. das können meines Erachtens wenige Explorer/Produzenten vorweisen ..

29.09.2015 Alkane Resources (ASX:ALK) has signed an agreement with global minerals and metals processing technology supplier Outotec to conduct an Early Contractor Involvement process for the Dubbo Zirconia Project (DZP) in New South Wales.

This is a key step in development of the project and will aid compilation of the financing package. DZP is expected to generate annual revenue of $580 million delivering EBITDA of $320 million and a 20-year NPV of $1.22 billion.

.....

Discussions on the financing are advancing and are run in parallel and in conjunction with completing product off-take agreements.

Alkane remains well-funded with A$14.8 million in cash at the end of June 2015, along with A$4.8 million in bullion and no debt.

Aktuelle MCAP 100 Mio A$. Bei aktuellen Goldpreisen von 1600 A$ und Produktionskosten von ~1200A$ und Produktion von 60-70000oz bleiben hier 20 Mio über, keine Schulden, die aktuellen Überschüsse aus dem Goldprojekt fließen in die Entwicklung des DZP Projekts, interessant wird hier die Finanzierung von 1,3 Mrd welche für das Projekt notwendig ist, aber über staatliche Mittel, oder einen Teilverkauf (10-20%) des Projekts finanziert werden soll, eine KE soll erst bei deutlich höheren Kursen durchgefüht werden, .. ich finde es spannend. Aktuell allerdings fast kein Handel, selbst in AUS gehen nur 50-300.000 Stk um ..

Viel Erfolg, werde hier mal wieder mehr mitlesen 8)

http://www.caesarsreport.com/blog/inca-one-is-still-working-hard-to-boost-its-margins-and-engages-jett-capital/

[url=http://peketec.de/trading/viewtopic.php?p=1627956#1627956 schrieb:Rookie schrieb am 29.09.2015, 08:43 Uhr[/url]"]Mit den Schulden hast Du nicht ganz unrecht, aber die Anlage und das zu verarbeitende Material mussten erstmal finanziert werden.

Es muss unbedingt die Grossmarge verbessert werden, das haben sie jetzt durch den Ankauf der Desorptionsanlage verbessert. Auch die Ausbringung und die Qualität des Ankaufmaterials werden sie erhöhen.

Ohne Ausweitung der Verarbeitung können sie nicht die OPEX abdecken.

Gross Marge 131.142 CAD, OPEX 3,6 Mill. CAD.

Darum stehen sie im Kurs momentan dort.

Bisher wurden sie von einer Schweizer Gruppe finanziert, die letzte Finanzierung lief als Gypsy swap ab.

Aber vielleicht habe ich etwas übersehen, bin immer an anderen Meinungen interessiert.

[url=http://peketec.de/trading/viewtopic.php?p=1627882#1627882 schrieb:Kostolanys Erbe schrieb am 28.09.2015, 22:44 Uhr[/url]"]Da bin ich persönlich anderer Meinung.

Ich sehe bei IO nur Schulden und dann evtl. bald neue Schulden die dazu kommen!

[url=http://peketec.de/trading/viewtopic.php?p=1627830#1627830 schrieb:Rookie schrieb am 28.09.2015, 18:31 Uhr[/url]"]sollte eigentlich besser dastehen, bisher sehr solide aufgebaut.

IRW-News: Inca One Gold Corp.: INCA ONE engagiert Jett Capital Advisors zur Beschaffung von Geldmitteln in Höhe von bis zu 20 Mio. USD für Betriebserweiterung

http://www.finanzen.net/nachricht/aktien/IRW-News-Inca-One-Gold-Corp-INCA-ONE-engagiert-Jett-Capital-Advisors-zur-Beschaffung-von-Geldmitteln-in-Hoehe-von-bis-zu-20-Mio-USD-fuer-Betriebserweiterung-4535097

Kostolanys Erbe

RohstoffExperte

Ort:

Im schönsten Bundesland zwischen Nord- und Ostsee.

Beiträge:

11.152

Trades:

4

Nachtrag:

BTT

Bitterroot agreement with Altius Minerals

2015-09-28 20:27 ET - Property Agreement

The TSX Venture Exchange has accepted documentation in connection with an agreement between Bitterroot Resources Ltd. and Altius Resources Inc., a wholly owned subsidiary of Altius Minerals Corp., pursuant to which Altius will finance future mineral exploration on Bitterroot's Voyageur lands and Copper Range lands in the Upper Peninsula of Michigan. Altius will pay $400,000 to Bitterroot and will commit to finance $600,000 of exploration expenditures on the properties within one year of the closing date of the transaction. Bitterroot will manage the first year's exploration program. In consideration for the foregoing payments and exploration expenditures, Altius will receive 50.1 per cent of the outstanding shares of Trans Superior Resources Inc., Bitterroot's wholly owned subsidiary which holds the properties, plus approximately four million common shares of Bitterroot, to be issued after Bitterroot completes a 1:10 consolidation.

Altius will also have the right to acquire an additional 19.9 per cent of Trans Superior by completing $2.5-million in exploration spending on the properties by the sixth anniversary of the closing date, plus the right to acquire an additional 10 per cent of Trans Superior by completing exploration spending of a further $5-million, or completing a National Instrument 43-101 prefeasibility study on a mineral resource on the properties, by the 10th anniversary of the closing date. Trans Superior will also grant to Altius a 2-per-cent net smelter return royalty on the Voyageur lands (covering approximately 250 square miles of mineral rights) and will also assign to Altius its right to purchase a 1-per-cent NSR held by a third party on the Copper Range lands.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313966&symbol=BTT®ion=C

Bitterroot Resources 1:10 rollback

2015-09-28 20:29 ET - Rollback

Pursuant to a special resolution passed by directors on Sept. 22, 2015, Bitterroot Resources Ltd. has consolidated its capital on a 1:10 basis. The name of Bitterroot has not been changed.

Effective at the opening on Tuesday, Sept. 29, 2015, the common shares of Bitterroot will commence trading on the TSX Venture Exchange on a consolidated basis. The company is classified as a mining exploration/development company.

Postconsolidation

Capitalization: unlimited shares with no par value of which 13,230,832 shares are issued and outstanding

Transfer agent: Computershare Investor Services Inc.

Symbol: BTT (unchanged)

New Cusip No.: 091901207

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313967&symbol=BTT®ion=C

Bitterroot Resources 3,077,022 shares for debt

2015-09-28 20:36 ET - Shares for Debt

The TSX Venture Exchange has accepted for filing Bitterroot Resources Ltd.'s proposal to issue 3,077,022 postconsolidated shares at a deemed price of 10 cents per share to settle outstanding debt for $307,702.65.

Creditors: 12

INSIDERS

Amount Price Shares

Barbara Carr $5,756.42 $0.10 57,564

Michael Carr $21,456.12 $0.10 214,561

Barbara Carr $146,875.56 $0.10 1,468,755

The company shall issue a news release when the shares are issued and the debt extinguished.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313969&symbol=BTT®ion=C

Bitterroot Resources 4,051,514-share private placement

2015-09-28 20:33 ET - Private Placement

The TSX Venture Exchange has accepted for filing documentation with respect to a non-brokered private placement announced June 22, 2015.

Shares: 4,051,514 postconsolidated shares

Price: 9.8729 cents

Placees: one

Insider: Altius Investments Ltd. 4,051,514

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313968&symbol=BTT®ion=C

BTT

Bitterroot agreement with Altius Minerals

2015-09-28 20:27 ET - Property Agreement

The TSX Venture Exchange has accepted documentation in connection with an agreement between Bitterroot Resources Ltd. and Altius Resources Inc., a wholly owned subsidiary of Altius Minerals Corp., pursuant to which Altius will finance future mineral exploration on Bitterroot's Voyageur lands and Copper Range lands in the Upper Peninsula of Michigan. Altius will pay $400,000 to Bitterroot and will commit to finance $600,000 of exploration expenditures on the properties within one year of the closing date of the transaction. Bitterroot will manage the first year's exploration program. In consideration for the foregoing payments and exploration expenditures, Altius will receive 50.1 per cent of the outstanding shares of Trans Superior Resources Inc., Bitterroot's wholly owned subsidiary which holds the properties, plus approximately four million common shares of Bitterroot, to be issued after Bitterroot completes a 1:10 consolidation.

Altius will also have the right to acquire an additional 19.9 per cent of Trans Superior by completing $2.5-million in exploration spending on the properties by the sixth anniversary of the closing date, plus the right to acquire an additional 10 per cent of Trans Superior by completing exploration spending of a further $5-million, or completing a National Instrument 43-101 prefeasibility study on a mineral resource on the properties, by the 10th anniversary of the closing date. Trans Superior will also grant to Altius a 2-per-cent net smelter return royalty on the Voyageur lands (covering approximately 250 square miles of mineral rights) and will also assign to Altius its right to purchase a 1-per-cent NSR held by a third party on the Copper Range lands.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313966&symbol=BTT®ion=C

Bitterroot Resources 1:10 rollback

2015-09-28 20:29 ET - Rollback

Pursuant to a special resolution passed by directors on Sept. 22, 2015, Bitterroot Resources Ltd. has consolidated its capital on a 1:10 basis. The name of Bitterroot has not been changed.

Effective at the opening on Tuesday, Sept. 29, 2015, the common shares of Bitterroot will commence trading on the TSX Venture Exchange on a consolidated basis. The company is classified as a mining exploration/development company.

Postconsolidation

Capitalization: unlimited shares with no par value of which 13,230,832 shares are issued and outstanding

Transfer agent: Computershare Investor Services Inc.

Symbol: BTT (unchanged)

New Cusip No.: 091901207

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313967&symbol=BTT®ion=C

Bitterroot Resources 3,077,022 shares for debt

2015-09-28 20:36 ET - Shares for Debt

The TSX Venture Exchange has accepted for filing Bitterroot Resources Ltd.'s proposal to issue 3,077,022 postconsolidated shares at a deemed price of 10 cents per share to settle outstanding debt for $307,702.65.

Creditors: 12

INSIDERS

Amount Price Shares

Barbara Carr $5,756.42 $0.10 57,564

Michael Carr $21,456.12 $0.10 214,561

Barbara Carr $146,875.56 $0.10 1,468,755

The company shall issue a news release when the shares are issued and the debt extinguished.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313969&symbol=BTT®ion=C

Bitterroot Resources 4,051,514-share private placement

2015-09-28 20:33 ET - Private Placement

The TSX Venture Exchange has accepted for filing documentation with respect to a non-brokered private placement announced June 22, 2015.

Shares: 4,051,514 postconsolidated shares

Price: 9.8729 cents

Placees: one

Insider: Altius Investments Ltd. 4,051,514

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aBTT-2313968&symbol=BTT®ion=C

Kostolanys Erbe

RohstoffExperte

Ort:

Im schönsten Bundesland zwischen Nord- und Ostsee.

Beiträge:

11.152

Trades:

4

AU:CAS

Crusader Resources mit news:

ASX RELEASE 29 Sep 2015

Juruena Maiden Resources include 178koz at >12 g/t Gold

http://www.crusaderresources.com/wp-content/uploads/2015/09/290915-Juruena-Maiden-Resource-FINAL.pdf

Crusader Resources mit news:

ASX RELEASE 29 Sep 2015

Juruena Maiden Resources include 178koz at >12 g/t Gold

http://www.crusaderresources.com/wp-content/uploads/2015/09/290915-Juruena-Maiden-Resource-FINAL.pdf

Kostolanys Erbe

RohstoffExperte

Ort:

Im schönsten Bundesland zwischen Nord- und Ostsee.

Beiträge:

11.152

Trades:

4

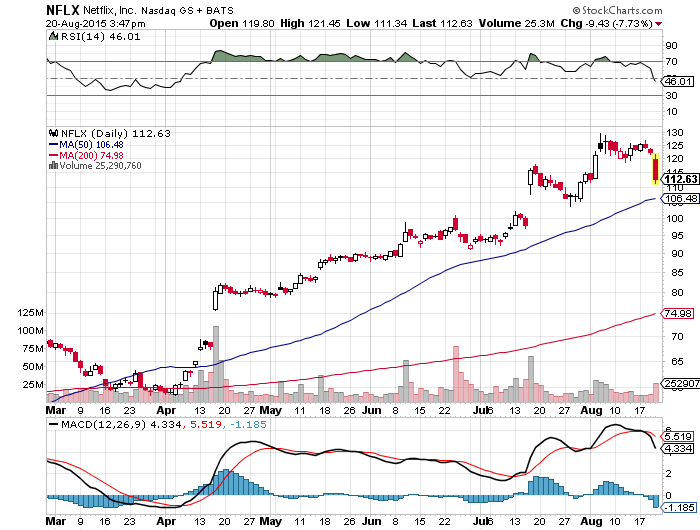

Anscheinend ist der Deckel erst mal nach oben die 100 $ Marke...

Infinera an einer wichtigen horizontalen Unterstützungslinie:

Infinera an einer wichtigen horizontalen Unterstützungslinie:

[url=http://peketec.de/trading/viewtopic.php?p=1622038#1622038 schrieb:Kostolanys Erbe schrieb am 09.09.2015, 17:48 Uhr[/url]"]Ein anderer Wert neben NFLX, wo sich charttechnisch eine S-K-S Formation bildet ist INFN und hat um die 14 US-Dollar noch ein Gap zu schliessen!

]» zur Grafik

Sept 9, 2015

Netflix readies for launch in Hong Kong, other Asian markets

Netflix shares jump more than 6% on news of Asia Expansion

http://www.marketwatch.com/story/netflix-readies-for-launch-in-hong-kong-other-asian-markets-2015-09-09?siteid=bigcharts&dist=bigcharts

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1619399#1619399 schrieb:Kostolanys Erbe schrieb am 31.08.2015, 20:51 Uhr[/url]"]Montag, 31.08.2015 - 17:52 Uhr

NETFLIX - Das Gap ruft

http://www.godmode-trader.de/analyse/netflix-das-gap-ruft,4323140

[/quote[url=http://peketec.de/trading/viewtopic.php?p=1618671#1618671 schrieb:Kostolanys Erbe schrieb am 27.08.2015, 23:28 Uhr[/url]"]Scheinchen CW2T7E klebt wieder am Lapi...

NFLX könnte charttechnisch um die 117-120 US$ die rechte Schulter einer SKS Formation ausbilden....?! Beobachten !!!

» zur Grafik

CEO hat schnell noch mal schön abgesahnt und seine Aktienoptionen versilbert...

und hält aktuell nicht mal eine Aktie seines Unternehmens !!!Ganz schön traurig... Wieviel Optionen er noch einlösen kann, weiss ich nicht...

» zur Grafik

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1617276#1617276 schrieb:Kostolanys Erbe schrieb am 24.08.2015, 21:16 Uhr[/url]"]@Olli

[url=http://peketec.de/trading/viewtopic.php?p=1616804#1616804 schrieb:Ollinho schrieb am 24.08.2015, 10:24 Uhr[/url]"]GW Kosto!!

[url=http://peketec.de/trading/viewtopic.php?p=1616774#1616774 schrieb:Kostolanys Erbe schrieb am 24.08.2015, 09:40 Uhr[/url]"]Verkauf zu 0,92 € !!!")

Börse heisst spekulieren und auch mal Gewinne mitnehmen!

Bin heute Abend mal auf die letzte Handelsstunde in USA gespannt...

[url=http://peketec.de/trading/viewtopic.php?p=1616461#1616461 schrieb:Kostolanys Erbe schrieb am 21.08.2015, 21:30 Uhr[/url]"]Danke @Olli

Scheinchen aktuell bei 0,72 €

https://www.boerse-stuttgart.de/de/boersenportal/wertpapiere-und-maerkte/hebelprodukte/optionsscheine/factsheet/?ID_NOTATION=137310115

NFLX aktuell die 50-Tage-Linie nach unten durchbrochen

Immer noch viel Speck drauf...

Und so langsam werden die die auf Margin debts zocken

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1616040#1616040 schrieb:Ollinho schrieb am 20.08.2015, 22:22 Uhr[/url]"]Sauber Kosto!!!

[url=http://peketec.de/trading/viewtopic.php?p=1616023#1616023 schrieb:Kostolanys Erbe schrieb am 20.08.2015, 21:50 Uhr[/url]"]

200-Tage-Linie bei ca. 75 $ !!!

Scheinchen steht aktuell bei 0,57 €

https://www.boerse-stuttgart.de/de/boersenportal/wertpapiere-und-maerkte/hebelprodukte/optionsscheine/factsheet/?ID_NOTATION=137310115

» zur Grafik

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1615368#1615368 schrieb:Kostolanys Erbe schrieb am 19.08.2015, 11:01 Uhr[/url]"]Kleine Put Speku-Posi CW2T7E zu 0,43€ genommen.

[url=http://peketec.de/trading/viewtopic.php?p=1615208#1615208 schrieb:Kostolanys Erbe schrieb am 18.08.2015, 22:40 Uhr[/url]"]Mich reizt ja irgendwie als Gapi-Freak ein Put (normalen OS / Kein Knock-out-Scheinchen in dieser Situation); Bewertung ist echt krass, irgendwann werden auch mal die von NFLX evtl. ein Quartal enttäuschen

» zur Grafik

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Kostolanys Erbe

RohstoffExperte

Ort:

Im schönsten Bundesland zwischen Nord- und Ostsee.

Beiträge:

11.152

Trades:

4

Atico drills 59.8 m of 5.74% Cu, two g/t Au at El Roble

2015-09-29 10:19 ET - News Release

Mr. Fernando Ganoza reports

ATICO INTERCEPTS 59.8M OF 5.74% CU AND 2.00G/T AU AT EL ROBLE MINE IN COLOMBIA

Atico Mining Corp. has released continuing infill drilling results at the El Roble mine that continue to extend mineralization at Zeus, at strike and approximately perpendicular to the strike direction of the massive sulphide body. In addition, the company reports the results for five diamond drill core holes (ATD-0015 through ATD-0019), which included 59.8 metres of 5.74 per cent copper and two grams per tonne gold.

Fernando E. Ganoza, chief executive officer, commented: "We are extremely pleased with the continued success of our infill drilling at El Roble. Drilling continued to intercept high-grade mineralization at the Zeus-Aquiles-Ares massive sulphide body and extending the mineralization beyond the previously outlined mineralized shell." Mr. Ganoza added, "With the tremendous success of this drill program to date, management has made the decision to use the last reported hole in this news release (ATD-0019) as the cutoff hole for the new resource update planned to be released before the end of this year. Production drilling will continue in the Zeus-Aquiles-Ares mineralization area while the exploration team will shift its focus on the perspective areas along strike and down dip."

EL ROBLE DRILLING HIGHLIGHTS

From To Interval Cu Au Ag

Hole (m) (m) (m) (%) (g/t) (g/t)

ATD-0017 175.80 235.60 59.80 5.74 2.00 9.48

Including 211.65 235.60 23.95 11.51 0.65 3.38

ATD-0019 201.30 252.00 50.70 0.51 3.52 10.85

Including 237.60 244.80 7.20 0.87 8.45 23.71

True widths are dependent on uncertainties in the local strike and dip of the mineralization, and are estimated to be between 64 per cent and 75 per cent of the drill intercept.

Infill drilling program

The goal of the current underground drilling program at the El Roble mine is to further define the known mineralized bodies and expand the identified resource. During the fourth quarter of 2014, the company began a drill program to specifically test the Zeus, Aquiles and Ares mineralized bodies. Infill drilling approximately perpendicular to the strike direction of the known massive sulphide bodies (318 degrees average strike, 85 degrees east average dip) and drilling of new prospective areas below the 2,000-metre level is being conducted from the new main level 1,880-metre adit. Subsequent to the five holes of the program (ATD-0010 to ATD-0014) where drilling significantly extended mineralization at Zeus and Aquiles as reported in June, 2015, (see Atico news release dated June 23, 2015), the company is reporting the next batch of five drill holes (ATD-0015 to ATD-0019). Infill hole ATD-0017 intercepted a completely new area of mineralization extending the massive sulphide body along strike to the south and to the west than had been modeled in the National Instrument 43-101 inferred resource estimate wireframes of Zeus, Aquiles and Ares (see Atico technical report dated Aug. 27, 2013).

An image, available on the company's website, clearly shows the strong mineralized infill intervals between the Aquiles and Ares mineralized bodies relative to previous drilling and to the west of the Zeus mineralized body. The mineralization remains open to southwest and down dip.

Exploration drilling program

Following the conclusion of Zeus-Aquiles-Ares infill program, the company is preparing for a new underground drill program designed to test the perspective areas at strike and down dip of the known mineralization. The results to date show that in proximity to the new prospective areas Cu-Au ratios are increasing both to the south and down dip in Zeus and Aquiles, and down dip Goliath and Maximus. Both patterns suggest that additional mineralization may exist down dip of Goliath and Maximus and south, as well as down dip of Zeus and Aquiles. This hypothesis is strengthened by the massive sulphide intercept in ATDHR-13 (see Atico news release dated Nov. 1, 2012) approximately 50 metres down dip of Maximus mineralized body. In addition, these areas are showing favorable geochemical and the structural geology results within the black chert host rock pointing to the possibility of hosting additional mineralization.

INFILL DRILL PROGRAM ASSAY Results

Intercept(i)

Total

Azimuth Dip Length From To Interval Cu Au Ag

Hole ID (degrees) (degrees) (m) (m) (m) (m) (%) (g/t) (g/t)

ATD-0015

37 -41 274.4 173.85 179.95 6.10 3.83 3.80 23.08

205.05 208.80 3.75 0.49 8.61 52.90

220.20 243.60 23.40 1.09 1.65 12.67

251.85 259.00 7.15 1.66 1.11 3.43

265.30 266.95 1.65 1.89 2.84 14.90

270.20 274.40 4.20 0.45 0.49 6.49

ATD-0016 41 -36 295.5 165.80 179.85 14.05 7.39 1.94 3.11

185.00 195.10 10.10 3.15 0.51 1.14

209.20 214.90 5.70 0.92 0.58 1.42

220.65 224.40 3.75 2.69 0.22 1.67

235.90 243.55 7.65 3.68 0.60 4.66

ATD-0017 44 -43 289.7 175.80 235.60 59.80 5.74 2.00 9.48

Including 178.40 181.30 2.90 4.62 10.20 33.27

203.30 210.85 7.55 5.55 0.72 5.68

211.65 235.60 23.95 11.51 0.65 3.38

ATD-0018 Failed due to a technical malfunction

ATD-0019 9 -30 283.35 201.30 252.00 50.70 0.51 3.52 10.85

Including 237.60 244.80 7.20 0.87 8.45 23.71

(i) True widths are dependent on uncertainties in the local strike and dip of

the mineralization, and are estimated to be between 64 per cent and 76 per cent

of the drill intercept.

(ii) Between the reported intervals for holes 15 and 16, there is disseminated

mineralization.

El Roble mine

The El Roble mine is a high-grade underground copper and gold mine with nominal processing plant capacity of 650 tonnes per day, located in the Department of Choco in Colombia. Its commercial product is a copper-gold concentrate.

Since obtaining control of the mine on Nov. 22, 2013, Atico has upgraded the operation from a nominal capacity of 400 tonnes per day. The mine has a continuous operating history of 22 years, with recorded production of 1.5 million tonnes of ore at an average head grade of 2.6 per cent copper and an estimated gold grade of 2.5 grams per tonne. Copper and gold mineralization at the El Roble property occurs in volcanogenic massive sulfide (VMS) lenses.

Since entering into the option agreement in January, 2011, to acquire 90 per cent of El Roble, Atico has aggressively explored the mine and surrounding claims. The company has completed 11,740 metres of diamond drilling and identified numerous prospective targets for VMS deposits on the 6,679-hectare property. This exploration led to the discovery of high-grade copper and gold mineralization below the 2,000-metre level, the lowest production level of the El Roble mine. Atico has developed a new adit access from the 1,880-metre elevation to develop these new resources.

Inferred mineral resource of 1.58 million tonnes grading 4.45 per cent copper and 3.17 grams per tonne gold, at a cut-off grade of 0.72 per cent copper equivalent (see Atico technical report dated Aug. 27, 2013). Mineralization is open at depth and along strike, and the company plans to further test the limits of the resource.

On the larger land package, the company has identified a prospective stratigraphic contact between volcanic rocks and black and grey cherts that has been traced by Atico geologists for 10 kilometres. This contact has been determined to be an important control on VMS mineralization on which Atico has identified 15 prospective target areas for VMS-type mineralization occurrence, which is the focus of the surface drill program at El Roble.

Quality assurance and quality control

Following detailed geological and geotechnical logging, drill core samples are split on-site with a diamond saw by Atico personnel. The seven to 10 kilograms per metre of sample are submitted to the ALS Chemex laboratory in Medellin where they are dried, crushed and pulverized. After preparation, the samples are sent to ALS Chemex in Lima and assayed. The remaining half-core sample is retained on-site for verification and reference purposes. All gold assays were obtained by standard 50-gram fire assay with AA finish. All copper and silver assays reported were obtained by aqua-regia sample dissolution of the sample followed by ICP analysis. The QA-QC program includes the blind insertion of certified reference standards as well as assay blanks and duplicates at a frequency of approximately one per 15 samples.

Qualified control

Dr. Demetrius Pohl, PhD, AIPG certified geologist, a qualified person under National Instrument 43-101 standards and independent of the company, is responsible for ensuring that the information contained in this news release is an accurate summary of the original reports and data provided to or developed by Atico Mining Corp. Dr. Pohl has approved the scientific and technical content of this news release.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aATY-2314130&symbol=ATY®ion=C

2015-09-29 10:19 ET - News Release

Mr. Fernando Ganoza reports

ATICO INTERCEPTS 59.8M OF 5.74% CU AND 2.00G/T AU AT EL ROBLE MINE IN COLOMBIA

Atico Mining Corp. has released continuing infill drilling results at the El Roble mine that continue to extend mineralization at Zeus, at strike and approximately perpendicular to the strike direction of the massive sulphide body. In addition, the company reports the results for five diamond drill core holes (ATD-0015 through ATD-0019), which included 59.8 metres of 5.74 per cent copper and two grams per tonne gold.

Fernando E. Ganoza, chief executive officer, commented: "We are extremely pleased with the continued success of our infill drilling at El Roble. Drilling continued to intercept high-grade mineralization at the Zeus-Aquiles-Ares massive sulphide body and extending the mineralization beyond the previously outlined mineralized shell." Mr. Ganoza added, "With the tremendous success of this drill program to date, management has made the decision to use the last reported hole in this news release (ATD-0019) as the cutoff hole for the new resource update planned to be released before the end of this year. Production drilling will continue in the Zeus-Aquiles-Ares mineralization area while the exploration team will shift its focus on the perspective areas along strike and down dip."

EL ROBLE DRILLING HIGHLIGHTS

From To Interval Cu Au Ag

Hole (m) (m) (m) (%) (g/t) (g/t)

ATD-0017 175.80 235.60 59.80 5.74 2.00 9.48

Including 211.65 235.60 23.95 11.51 0.65 3.38

ATD-0019 201.30 252.00 50.70 0.51 3.52 10.85

Including 237.60 244.80 7.20 0.87 8.45 23.71

True widths are dependent on uncertainties in the local strike and dip of the mineralization, and are estimated to be between 64 per cent and 75 per cent of the drill intercept.

Infill drilling program

The goal of the current underground drilling program at the El Roble mine is to further define the known mineralized bodies and expand the identified resource. During the fourth quarter of 2014, the company began a drill program to specifically test the Zeus, Aquiles and Ares mineralized bodies. Infill drilling approximately perpendicular to the strike direction of the known massive sulphide bodies (318 degrees average strike, 85 degrees east average dip) and drilling of new prospective areas below the 2,000-metre level is being conducted from the new main level 1,880-metre adit. Subsequent to the five holes of the program (ATD-0010 to ATD-0014) where drilling significantly extended mineralization at Zeus and Aquiles as reported in June, 2015, (see Atico news release dated June 23, 2015), the company is reporting the next batch of five drill holes (ATD-0015 to ATD-0019). Infill hole ATD-0017 intercepted a completely new area of mineralization extending the massive sulphide body along strike to the south and to the west than had been modeled in the National Instrument 43-101 inferred resource estimate wireframes of Zeus, Aquiles and Ares (see Atico technical report dated Aug. 27, 2013).

An image, available on the company's website, clearly shows the strong mineralized infill intervals between the Aquiles and Ares mineralized bodies relative to previous drilling and to the west of the Zeus mineralized body. The mineralization remains open to southwest and down dip.

Exploration drilling program

Following the conclusion of Zeus-Aquiles-Ares infill program, the company is preparing for a new underground drill program designed to test the perspective areas at strike and down dip of the known mineralization. The results to date show that in proximity to the new prospective areas Cu-Au ratios are increasing both to the south and down dip in Zeus and Aquiles, and down dip Goliath and Maximus. Both patterns suggest that additional mineralization may exist down dip of Goliath and Maximus and south, as well as down dip of Zeus and Aquiles. This hypothesis is strengthened by the massive sulphide intercept in ATDHR-13 (see Atico news release dated Nov. 1, 2012) approximately 50 metres down dip of Maximus mineralized body. In addition, these areas are showing favorable geochemical and the structural geology results within the black chert host rock pointing to the possibility of hosting additional mineralization.

INFILL DRILL PROGRAM ASSAY Results

Intercept(i)

Total

Azimuth Dip Length From To Interval Cu Au Ag

Hole ID (degrees) (degrees) (m) (m) (m) (m) (%) (g/t) (g/t)

ATD-0015

37 -41 274.4 173.85 179.95 6.10 3.83 3.80 23.08

205.05 208.80 3.75 0.49 8.61 52.90

220.20 243.60 23.40 1.09 1.65 12.67

251.85 259.00 7.15 1.66 1.11 3.43

265.30 266.95 1.65 1.89 2.84 14.90

270.20 274.40 4.20 0.45 0.49 6.49

ATD-0016 41 -36 295.5 165.80 179.85 14.05 7.39 1.94 3.11

185.00 195.10 10.10 3.15 0.51 1.14

209.20 214.90 5.70 0.92 0.58 1.42

220.65 224.40 3.75 2.69 0.22 1.67

235.90 243.55 7.65 3.68 0.60 4.66

ATD-0017 44 -43 289.7 175.80 235.60 59.80 5.74 2.00 9.48

Including 178.40 181.30 2.90 4.62 10.20 33.27

203.30 210.85 7.55 5.55 0.72 5.68

211.65 235.60 23.95 11.51 0.65 3.38

ATD-0018 Failed due to a technical malfunction

ATD-0019 9 -30 283.35 201.30 252.00 50.70 0.51 3.52 10.85

Including 237.60 244.80 7.20 0.87 8.45 23.71

(i) True widths are dependent on uncertainties in the local strike and dip of

the mineralization, and are estimated to be between 64 per cent and 76 per cent

of the drill intercept.

(ii) Between the reported intervals for holes 15 and 16, there is disseminated

mineralization.

El Roble mine

The El Roble mine is a high-grade underground copper and gold mine with nominal processing plant capacity of 650 tonnes per day, located in the Department of Choco in Colombia. Its commercial product is a copper-gold concentrate.

Since obtaining control of the mine on Nov. 22, 2013, Atico has upgraded the operation from a nominal capacity of 400 tonnes per day. The mine has a continuous operating history of 22 years, with recorded production of 1.5 million tonnes of ore at an average head grade of 2.6 per cent copper and an estimated gold grade of 2.5 grams per tonne. Copper and gold mineralization at the El Roble property occurs in volcanogenic massive sulfide (VMS) lenses.

Since entering into the option agreement in January, 2011, to acquire 90 per cent of El Roble, Atico has aggressively explored the mine and surrounding claims. The company has completed 11,740 metres of diamond drilling and identified numerous prospective targets for VMS deposits on the 6,679-hectare property. This exploration led to the discovery of high-grade copper and gold mineralization below the 2,000-metre level, the lowest production level of the El Roble mine. Atico has developed a new adit access from the 1,880-metre elevation to develop these new resources.

Inferred mineral resource of 1.58 million tonnes grading 4.45 per cent copper and 3.17 grams per tonne gold, at a cut-off grade of 0.72 per cent copper equivalent (see Atico technical report dated Aug. 27, 2013). Mineralization is open at depth and along strike, and the company plans to further test the limits of the resource.

On the larger land package, the company has identified a prospective stratigraphic contact between volcanic rocks and black and grey cherts that has been traced by Atico geologists for 10 kilometres. This contact has been determined to be an important control on VMS mineralization on which Atico has identified 15 prospective target areas for VMS-type mineralization occurrence, which is the focus of the surface drill program at El Roble.

Quality assurance and quality control

Following detailed geological and geotechnical logging, drill core samples are split on-site with a diamond saw by Atico personnel. The seven to 10 kilograms per metre of sample are submitted to the ALS Chemex laboratory in Medellin where they are dried, crushed and pulverized. After preparation, the samples are sent to ALS Chemex in Lima and assayed. The remaining half-core sample is retained on-site for verification and reference purposes. All gold assays were obtained by standard 50-gram fire assay with AA finish. All copper and silver assays reported were obtained by aqua-regia sample dissolution of the sample followed by ICP analysis. The QA-QC program includes the blind insertion of certified reference standards as well as assay blanks and duplicates at a frequency of approximately one per 15 samples.

Qualified control

Dr. Demetrius Pohl, PhD, AIPG certified geologist, a qualified person under National Instrument 43-101 standards and independent of the company, is responsible for ensuring that the information contained in this news release is an accurate summary of the original reports and data provided to or developed by Atico Mining Corp. Dr. Pohl has approved the scientific and technical content of this news release.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aATY-2314130&symbol=ATY®ion=C

Kostolanys Erbe

RohstoffExperte

Ort:

Im schönsten Bundesland zwischen Nord- und Ostsee.

Beiträge:

11.152

Trades:

4

Insidergeschäfte BSX:

Sep 28/15 Sep 25/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 358,000 $0.184

Sep 23/15 Sep 22/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 101,000 $0.180

Sep 23/15 Sep 22/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 2,268,949 $0.175

Sep 22/15 Sep 21/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 16,500 $0.180

Sep 22/15 Sep 18/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 13,500 $0.183

Aug 25/15 Aug 21/15 Eaton, Mark Price Direct Ownership Common Shares 10 - Acquisition in the public market 300,000 $19.35

Jul 28/15 Jul 24/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 264,500 $0.159

Jul 28/15 Jul 23/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 26,500 $0.160 -

https://www.canadianinsider.com/company?menu_tickersearch=bsx#sthash.ZqfP97wV.dpuf

Insidergeschäfte SBB:

Sep 28/15 Sep 28/15 Segsworth, Walter Thomas Direct Ownership Options 50 - Grant of options 100,000 $0.380

Sep 28/15 Sep 25/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 14,500 $0.380

Sep 25/15 Sep 24/15 Sun Valley Gold LLC Control or Direction Common Shares 10 - Acquisition in the public market 50,000 $0.385

Sep 18/15 Sep 18/15 McLeod, Donald Bruce Direct Ownership Common Shares 10 - Acquisition in the public market 25,000 $0.365

Sep 18/15 Sep 17/15 McLeod, Donald Bruce Direct Ownership Common Shares 10 - Acquisition in the public market 10,000 $0.355

Sep 18/15 Sep 17/15 McLeod, Donald Bruce Direct Ownership Common Shares 10 - Acquisition in the public market 30,000 $0.360

Sep 17/15 Sep 16/15 Goodman, Jonathan Carter Indirect Ownership Common Shares 11 - Acquisition carried out privately 200,000

Aug 28/15 Aug 27/15 John, William Murray Direct Ownership Common Shares 10 - Acquisition in the public market 150,000 $0.320

Aug 26/15 Aug 26/15 John, William Murray Direct Ownership Common Shares 10 - Acquisition in the public market 100,000 $0.320

Aug 26/15 Aug 25/15 John, William Murray Direct Ownership Common Shares 10 - Acquisition in the public market 50,000 $0.350 -

https://www.canadianinsider.com/company?menu_tickersearch=sbb#sthash.i1c9NXmt.dpuf

Seit langen mal wieder Insidergeschäfte (kleine ) bei CKG:

Sep 28/15 Sep 25/15 Reifel, P. Randy Direct Ownership Common Shares 10 - Acquisition in the public market 2,500 $1.40

Sep 24/15 Sep 21/15 Reifel, P. Randy Direct Ownership Common Shares 10 - Acquisition in the public market 2,500 $1.40

Sep 11/15 Sep 11/15 Reifel, P. Randy Indirect Ownership Common Shares 10 - Acquisition in the public market 5,000 $1.45

Sep 11/15 Sep 11/15 Reifel, P. Randy Indirect Ownership Common Shares 10 - Acquisition in the public market 5,000 $1.50

Sep 11/15 Sep 11/15 Reifel, P. Randy Indirect Ownership Common Shares 10 - Acquisition in the public market 5,000 $1.55 -

https://www.canadianinsider.com/company?menu_tickersearch=ckg#sthash.2E2Ldv5h.dpuf

ATY - mal wieder sehr gute Bohrergebnisse, im Moment lockt es niemanden hinterm Ofen hervor........

3 Umätze und im Minus geschlossen........hochgradige Kupfer+Goldmine, eigentlich eine Top-Kombination

müssen den operativen Turnaround packen.......dann geht auch der Kurs ab

3 Umätze und im Minus geschlossen........hochgradige Kupfer+Goldmine, eigentlich eine Top-Kombination

müssen den operativen Turnaround packen.......dann geht auch der Kurs ab

[url=http://peketec.de/trading/viewtopic.php?p=1628176#1628176 schrieb:Kostolanys Erbe schrieb am 29.09.2015, 21:00 Uhr[/url]"]Atico drills 59.8 m of 5.74% Cu, two g/t Au at El Roble

2015-09-29 10:19 ET - News Release

Mr. Fernando Ganoza reports

ATICO INTERCEPTS 59.8M OF 5.74% CU AND 2.00G/T AU AT EL ROBLE MINE IN COLOMBIA

Atico Mining Corp. has released continuing infill drilling results at the El Roble mine that continue to extend mineralization at Zeus, at strike and approximately perpendicular to the strike direction of the massive sulphide body. In addition, the company reports the results for five diamond drill core holes (ATD-0015 through ATD-0019), which included 59.8 metres of 5.74 per cent copper and two grams per tonne gold.

Fernando E. Ganoza, chief executive officer, commented: "We are extremely pleased with the continued success of our infill drilling at El Roble. Drilling continued to intercept high-grade mineralization at the Zeus-Aquiles-Ares massive sulphide body and extending the mineralization beyond the previously outlined mineralized shell." Mr. Ganoza added, "With the tremendous success of this drill program to date, management has made the decision to use the last reported hole in this news release (ATD-0019) as the cutoff hole for the new resource update planned to be released before the end of this year. Production drilling will continue in the Zeus-Aquiles-Ares mineralization area while the exploration team will shift its focus on the perspective areas along strike and down dip."

EL ROBLE DRILLING HIGHLIGHTS

From To Interval Cu Au Ag

Hole (m) (m) (m) (%) (g/t) (g/t)

ATD-0017 175.80 235.60 59.80 5.74 2.00 9.48

Including 211.65 235.60 23.95 11.51 0.65 3.38

ATD-0019 201.30 252.00 50.70 0.51 3.52 10.85

Including 237.60 244.80 7.20 0.87 8.45 23.71

.........................

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aATY-2314130&symbol=ATY®ion=C

ABX - Barrick mit zwei interessanten News nach Börsenschluss:

Nummer1:

Barrick closes $610M (U.S.) Au, Ag streaming deal

2015-09-29 17:15 ET - News Release

Mr. Kelvin Dushnisky reports

BARRICK CLOSES INNOVATIVE GOLD AND SILVER STREAMING TRANSACTION WITH ROYAL GOLD

Barrick Gold Corp. has closed its previously announced gold and silver streaming transaction with RGLD Gold AG, a wholly owned subsidiary of Royal Gold Inc., for production referenced to Barrick's 60-per-cent interest in the Pueblo Viejo mine. All amounts expressed in US dollars.

Barrick has received an upfront cash payment of $610 million and will receive continuing cash payments for gold and silver delivered under the agreement. Proceeds from the transaction will be used to reduce debt.

Distinctive characteristics of the agreement include:

Significant upside price participation for Barrick.

Not subject to a Barrick guarantee, and not treated as a debt-like obligation.

Obligation of Barrick to sell gold and silver under the agreement is serviced using after tax cash flow being remitted from the Dominican Republic.

Under the terms of the agreement, Barrick will sell gold and silver to Royal Gold equivalent to:

7.5 percent of Barrick's interest in the gold produced at Pueblo Viejo until 990,000 ounces of gold have been delivered, and 3.75 percent thereafter.

75 percent of Barrick's interest in the silver produced at Pueblo Viejo until 50 million ounces have been delivered, and 37.5 percent thereafter. Silver will be delivered based on a fixed recovery rate of 70 percent. Silver above this recovery rate is not subject to the stream.

Ongoing cash payments to Barrick are tied to prevailing spot prices rather than fixed in advance, maintaining material exposure to higher gold and silver prices in the future. Barrick will receive ongoing cash payments from Royal Gold equivalent to 30 percent of the prevailing spot prices for the first 550,000 ounces of gold and 23.1 million ounces of silver delivered. Thereafter payments will double to 60 percent of prevailing spot prices for each subsequent ounce of gold and silver delivered.

"This innovative agreement allows us to strengthen our balance sheet in the short term, while preserving material exposure to higher gold and silver prices in the future," said Barrick President Kelvin Dushnisky.

Barrick maintains its 60 percent equity ownership interest in Pueblo Viejo and its associated rights under the joint venture agreement with Goldcorp Inc., including operatorship of Pueblo Viejo. This transaction does not affect any of Pueblo Viejo's obligations to the Dominican Government.

We seek Safe Harbor.

© 2015 Canjex Publishing Ltd. All rights reserved.

Nummer1:

Barrick closes $610M (U.S.) Au, Ag streaming deal

2015-09-29 17:15 ET - News Release

Mr. Kelvin Dushnisky reports

BARRICK CLOSES INNOVATIVE GOLD AND SILVER STREAMING TRANSACTION WITH ROYAL GOLD

Barrick Gold Corp. has closed its previously announced gold and silver streaming transaction with RGLD Gold AG, a wholly owned subsidiary of Royal Gold Inc., for production referenced to Barrick's 60-per-cent interest in the Pueblo Viejo mine. All amounts expressed in US dollars.

Barrick has received an upfront cash payment of $610 million and will receive continuing cash payments for gold and silver delivered under the agreement. Proceeds from the transaction will be used to reduce debt.

Distinctive characteristics of the agreement include:

Significant upside price participation for Barrick.

Not subject to a Barrick guarantee, and not treated as a debt-like obligation.

Obligation of Barrick to sell gold and silver under the agreement is serviced using after tax cash flow being remitted from the Dominican Republic.

Under the terms of the agreement, Barrick will sell gold and silver to Royal Gold equivalent to:

7.5 percent of Barrick's interest in the gold produced at Pueblo Viejo until 990,000 ounces of gold have been delivered, and 3.75 percent thereafter.

75 percent of Barrick's interest in the silver produced at Pueblo Viejo until 50 million ounces have been delivered, and 37.5 percent thereafter. Silver will be delivered based on a fixed recovery rate of 70 percent. Silver above this recovery rate is not subject to the stream.

Ongoing cash payments to Barrick are tied to prevailing spot prices rather than fixed in advance, maintaining material exposure to higher gold and silver prices in the future. Barrick will receive ongoing cash payments from Royal Gold equivalent to 30 percent of the prevailing spot prices for the first 550,000 ounces of gold and 23.1 million ounces of silver delivered. Thereafter payments will double to 60 percent of prevailing spot prices for each subsequent ounce of gold and silver delivered.

"This innovative agreement allows us to strengthen our balance sheet in the short term, while preserving material exposure to higher gold and silver prices in the future," said Barrick President Kelvin Dushnisky.

Barrick maintains its 60 percent equity ownership interest in Pueblo Viejo and its associated rights under the joint venture agreement with Goldcorp Inc., including operatorship of Pueblo Viejo. This transaction does not affect any of Pueblo Viejo's obligations to the Dominican Government.

We seek Safe Harbor.

© 2015 Canjex Publishing Ltd. All rights reserved.

ABX - Barrick mit zwei interessanten News nach Börsenschluss:

Nummer 2:

http://www.marketwired.com/press-release/barrick-announces-debt-tender-offer-nyse-abx-2059541.htm

Barrick begins tender offer for outstanding notes

2015-09-29 17:28 ET - News Release

Mr. Andy Lloyd reports

BARRICK ANNOUNCES DEBT TENDER OFFER

Barrick Gold Corp. and certain of its subsidiaries have commenced a cash tender offer for specified series of outstanding notes. The terms and conditions of the tender offer are described in an offer to purchase and the related letter of transmittal, each dated today. (All amounts are expressed in U.S. dollars.)

The tender offer

Barrick, Barrick North America Finance LLC and Barrick (PD) Australia Finance Pty. Ltd. are offering to purchase for cash the series of notes set out in the attached table for an aggregate purchase price (including principal and premium) of up to $750-million, as such amount may be increased by the offerors, plus accrued and unpaid interest on the notes from the last applicable interest payment date up to, but not including, the settlement date. The amount of a series of notes that is purchased in the tender offer will be based on the order of priority (the acceptance priority level) for such series of notes as set forth in the attached table, with one being the highest acceptance priority level and seven being the lowest acceptance priority level. In addition, the aggregate principal amount relating to the offer to purchase the series of notes with acceptance priority Level 2 will be limited to $275-million (such principal amount, the Priority 2 tender cap). If there are sufficient remaining funds to purchase some, but not all, of the notes tendered of any series (other than the Priority 2 notes), the amount of notes purchased in that series will be subject to proration using the procedure more fully described in the offer to purchase. In addition, if Priority 2 notes are validly tendered and not validly withdrawn such that the aggregate principal amount to be purchased of such Priority 2 notes would exceed the Priority 2 tender cap, the amount of Priority 2 notes purchased will be subject to proration using the procedure more fully described in the offer to purchase.

Nummer 2:

http://www.marketwired.com/press-release/barrick-announces-debt-tender-offer-nyse-abx-2059541.htm

Barrick begins tender offer for outstanding notes

2015-09-29 17:28 ET - News Release

Mr. Andy Lloyd reports

BARRICK ANNOUNCES DEBT TENDER OFFER

Barrick Gold Corp. and certain of its subsidiaries have commenced a cash tender offer for specified series of outstanding notes. The terms and conditions of the tender offer are described in an offer to purchase and the related letter of transmittal, each dated today. (All amounts are expressed in U.S. dollars.)

The tender offer

Barrick, Barrick North America Finance LLC and Barrick (PD) Australia Finance Pty. Ltd. are offering to purchase for cash the series of notes set out in the attached table for an aggregate purchase price (including principal and premium) of up to $750-million, as such amount may be increased by the offerors, plus accrued and unpaid interest on the notes from the last applicable interest payment date up to, but not including, the settlement date. The amount of a series of notes that is purchased in the tender offer will be based on the order of priority (the acceptance priority level) for such series of notes as set forth in the attached table, with one being the highest acceptance priority level and seven being the lowest acceptance priority level. In addition, the aggregate principal amount relating to the offer to purchase the series of notes with acceptance priority Level 2 will be limited to $275-million (such principal amount, the Priority 2 tender cap). If there are sufficient remaining funds to purchase some, but not all, of the notes tendered of any series (other than the Priority 2 notes), the amount of notes purchased in that series will be subject to proration using the procedure more fully described in the offer to purchase. In addition, if Priority 2 notes are validly tendered and not validly withdrawn such that the aggregate principal amount to be purchased of such Priority 2 notes would exceed the Priority 2 tender cap, the amount of Priority 2 notes purchased will be subject to proration using the procedure more fully described in the offer to purchase.

Wie seht ihr die aktuellen Zahlen von D7Q1?

Ist die AG nicht absolut unterbewertet?

DGAP-News: Monument Mining Ltd.: Nettogewinn von 11 Mio. USD bei 0,04 USD pro Aktie mit Cash Cost von 587 USD pro Unze (deutsch)

Monument Mining Ltd.: Nettogewinn von 11 Mio. USD bei 0,04 USD pro Aktie mit Cash Cost von 587 USD pro Unze

DGAP-News: Monument Mining Ltd. / Schlagwort(e):

Jahresergebnis/Expansion

Monument Mining Ltd.: Nettogewinn von 11 Mio. USD bei 0,04 USD pro

Aktie mit Cash Cost von 587 USD pro Unze

30.09.2015 / 08:36

---------------------------------------------------------------------

Monument Mining gibt Ergebnisse des Geschäftsjahres 2015 bekannt

Nettogewinn von 11 Mio. USD bei 0,04 USD pro Aktie mit Cash Cost von 587

USD pro Unze

Vancouver, British Columbia, Kanada. 29. September 2015. Monument Mining

Limited (Frankfurt: WKN A0MSJR; TSX-V: MMY) ("Monument" oder das

"Unternehmen") gibt heute die Finanz- und Betriebsergebnisse für das

Geschäftsjahr mit Ende 30. Juni 2015 bekannt. Alle Beträge in US-Dollar,

falls nicht anders angegeben (siehe www.sedar.com für vollständige Fassung

des Jahresberichts).

Präsident und CEO Robert Baldock kommentierte die Produktions- und

Geschäftsergebnisse des Geschäftsjahres 2015: "Monument berichtet einen

Nettogewinn von 11,4 Mio. USD und einen Gewinn pro Aktie von 4 US-Cent.

Durch effiziente Nutzung der Ressourcen haben die Betriebe die

Produktivität und die Goldausbringungsraten erhöht. Unsere Bilanz ist

weiterhin solide und unsere Entwicklungsprogramme verwenden Innovationen

zum Aufbau und zur Entwicklung des Projektportfolios zur Steigerung der

Goldressourcen und der Ressourcen andere Buntmetalle für alle Stakeholder."

Die wichtigsten Punkte des Geschäftsjahres 2015:

- Nettogewinn erhöhte sich um 14,01 Mio. USD auf 11,38 Mio. USD bei 0,04

USD pro Aktie (2014: Nettoverlust von 2,63 Mio. oder (0,01 USD) pro

Aktie);

- Cash Cost pro Unze reduzierten sich um 4 % auf 587 USD pro Unze ("oz")

(2014: 613 USD/oz);

- Goldausbringung stieg um 12 % auf 36.567 oz (2014: 32.568 oz);

- Goldausbringungsrate stieg um 9 % auf 82,4 % (2014: 75,9 5);

- Gehalt des Fördererzes stieg um 11 % auf 1,45 g/t Au (2014: 1,31 g/t

Au);

- Gewinnmarge aus Goldproduktion von 15,89 Mio. USD (2014: 16,28 Mio.

USD);

- Verkauf von 36.500 oz Gold für Bruttoeinnahmen von 44,84 Mio. USD

(2014: 37.670 oz verkauft für 48,58 Mio. USD);

- einstweilige Lizenz von Intec gesichert zur Nutzung der

Ausbringungstechnologie für Gold und Kupfer aus Sulfiden;

- Bestätigung einer Goldressource auf Lagerstätten Alliance/New Alliance

("ANA") in Murchison mit einem bei SEDAR eingereichten NI 43-101

Bericht.

(News gekürtz abgebildet)

Ist die AG nicht absolut unterbewertet?

DGAP-News: Monument Mining Ltd.: Nettogewinn von 11 Mio. USD bei 0,04 USD pro Aktie mit Cash Cost von 587 USD pro Unze (deutsch)

Monument Mining Ltd.: Nettogewinn von 11 Mio. USD bei 0,04 USD pro Aktie mit Cash Cost von 587 USD pro Unze

DGAP-News: Monument Mining Ltd. / Schlagwort(e):

Jahresergebnis/Expansion

Monument Mining Ltd.: Nettogewinn von 11 Mio. USD bei 0,04 USD pro

Aktie mit Cash Cost von 587 USD pro Unze

30.09.2015 / 08:36

---------------------------------------------------------------------

Monument Mining gibt Ergebnisse des Geschäftsjahres 2015 bekannt

Nettogewinn von 11 Mio. USD bei 0,04 USD pro Aktie mit Cash Cost von 587

USD pro Unze

Vancouver, British Columbia, Kanada. 29. September 2015. Monument Mining

Limited (Frankfurt: WKN A0MSJR; TSX-V: MMY) ("Monument" oder das

"Unternehmen") gibt heute die Finanz- und Betriebsergebnisse für das

Geschäftsjahr mit Ende 30. Juni 2015 bekannt. Alle Beträge in US-Dollar,

falls nicht anders angegeben (siehe www.sedar.com für vollständige Fassung

des Jahresberichts).

Präsident und CEO Robert Baldock kommentierte die Produktions- und

Geschäftsergebnisse des Geschäftsjahres 2015: "Monument berichtet einen

Nettogewinn von 11,4 Mio. USD und einen Gewinn pro Aktie von 4 US-Cent.

Durch effiziente Nutzung der Ressourcen haben die Betriebe die

Produktivität und die Goldausbringungsraten erhöht. Unsere Bilanz ist

weiterhin solide und unsere Entwicklungsprogramme verwenden Innovationen

zum Aufbau und zur Entwicklung des Projektportfolios zur Steigerung der

Goldressourcen und der Ressourcen andere Buntmetalle für alle Stakeholder."

Die wichtigsten Punkte des Geschäftsjahres 2015:

- Nettogewinn erhöhte sich um 14,01 Mio. USD auf 11,38 Mio. USD bei 0,04

USD pro Aktie (2014: Nettoverlust von 2,63 Mio. oder (0,01 USD) pro

Aktie);

- Cash Cost pro Unze reduzierten sich um 4 % auf 587 USD pro Unze ("oz")

(2014: 613 USD/oz);

- Goldausbringung stieg um 12 % auf 36.567 oz (2014: 32.568 oz);

- Goldausbringungsrate stieg um 9 % auf 82,4 % (2014: 75,9 5);

- Gehalt des Fördererzes stieg um 11 % auf 1,45 g/t Au (2014: 1,31 g/t

Au);

- Gewinnmarge aus Goldproduktion von 15,89 Mio. USD (2014: 16,28 Mio.

USD);

- Verkauf von 36.500 oz Gold für Bruttoeinnahmen von 44,84 Mio. USD

(2014: 37.670 oz verkauft für 48,58 Mio. USD);

- einstweilige Lizenz von Intec gesichert zur Nutzung der

Ausbringungstechnologie für Gold und Kupfer aus Sulfiden;

- Bestätigung einer Goldressource auf Lagerstätten Alliance/New Alliance

("ANA") in Murchison mit einem bei SEDAR eingereichten NI 43-101

Bericht.

(News gekürtz abgebildet)

Ich bin hier mal für 0,069 EUR rein. Habe das Gefühl das der Kurs nach oben geht!

[url=http://peketec.de/trading/viewtopic.php?p=1628285#1628285 schrieb:greenhorn schrieb am 30.09.2015, 09:26 Uhr[/url]"]

MK bei 29 Mio CAD

In der Tat vollkommen ausgebombt, so gut wie kein Schulden und ordentlich Cash dazu!

[url=http://peketec.de/trading/view-topic.php?p=1628313#1628313 schrieb:ocram_I schrieb am 30.09.2015, 09:51 Uhr[/url]"]Ich bin hier mal für 0,069 EUR rein. Habe das Gefühl das der Kurs nach oben geht!

[url=http://peketec.de/trading/viewtopic.php?p=1628285#1628285 schrieb:greenhorn schrieb am 30.09.2015, 09:26 Uhr[/url]"]

MK bei 29 Mio CAD

Bei den letzten Jahreszahlen waren noch 2,6 Mio Nettoverlust ausgewiesen (0,01 USD/Aktie). Die aktuelle Steigerung kam auch nicht durch Sondereffekte zustande sondern durch Kosteneinsparungen usw.

[url=http://peketec.de/trading/viewtopic.php?p=1628345#1628345 schrieb:Fischlaender schrieb am 30.09.2015, 10:40 Uhr[/url]"]In der Tat vollkommen ausgebombt, so gut wie kein Schulden und ordentlich Cash dazu![url=http://peketec.de/trading/view-topic.php?p=1628313#1628313 schrieb:ocram_I schrieb am 30.09.2015, 09:51 Uhr[/url]"]Ich bin hier mal für 0,069 EUR rein. Habe das Gefühl das der Kurs nach oben geht!

[url=http://peketec.de/trading/viewtopic.php?p=1628285#1628285 schrieb:greenhorn schrieb am 30.09.2015, 09:26 Uhr[/url]"]

MK bei 29 Mio CAD

habe auch nach Sondereffekten gesucht, nicht s gefunden, sieht extrem günstig aus

"Geschäftsjahr 2014. Im vierten Quartal des Geschäftsjahres 2015 betrug der Cashflow aus dem Geschäftsbetrieb 3,52 Mio. USD verglichen mit 4,87 Mio. USD im vierten Quartal des Geschäftsjahres 2014. Zum 30. Juni 2015 verfügte das Unternehmen über ein Betriebskapital von 39,72 Mio. USD, eine Zunahme von 2,22 Mio. USD gegenüber den 37,05 Mio. USD zum 30. Juni 2014."

Ergebnis 0,04 $ je Aktie? bei einem Kurs von 0,09 $

Einzige was mir nicht so gefällt ist eine deutsche Website, spricht für irgendeine Empfehlungs-Brief-Geschichte (zumindest nicht selten so..)

"Geschäftsjahr 2014. Im vierten Quartal des Geschäftsjahres 2015 betrug der Cashflow aus dem Geschäftsbetrieb 3,52 Mio. USD verglichen mit 4,87 Mio. USD im vierten Quartal des Geschäftsjahres 2014. Zum 30. Juni 2015 verfügte das Unternehmen über ein Betriebskapital von 39,72 Mio. USD, eine Zunahme von 2,22 Mio. USD gegenüber den 37,05 Mio. USD zum 30. Juni 2014."

Ergebnis 0,04 $ je Aktie? bei einem Kurs von 0,09 $

Einzige was mir nicht so gefällt ist eine deutsche Website, spricht für irgendeine Empfehlungs-Brief-Geschichte (zumindest nicht selten so..)

[url=http://peketec.de/trading/viewtopic.php?p=1628349#1628349 schrieb:ocram_I schrieb am 30.09.2015, 10:50 Uhr[/url]"]Bei den letzten Jahreszahlen waren noch 2,6 Mio Nettoverlust ausgewiesen (0,01 USD/Aktie). Die aktuelle Steigerung kam auch nicht durch Sondereffekte zustande sondern durch Kosteneinsparungen usw.

[url=http://peketec.de/trading/viewtopic.php?p=1628345#1628345 schrieb:Fischlaender schrieb am 30.09.2015, 10:40 Uhr[/url]"]In der Tat vollkommen ausgebombt, so gut wie kein Schulden und ordentlich Cash dazu![url=http://peketec.de/trading/view-topic.php?p=1628313#1628313 schrieb:ocram_I schrieb am 30.09.2015, 09:51 Uhr[/url]"]Ich bin hier mal für 0,069 EUR rein. Habe das Gefühl das der Kurs nach oben geht!