Miranda Acquires Rights to Purchase 3.3% Royalty at Willow Creek and Extends Gold Torrent

https://www.accesswire.com/viewarticle.aspx?id=432891

https://www.accesswire.com/viewarticle.aspx?id=432891

Follow along with the video below to see how to install our site as a web app on your home screen.

Anmerkung: This feature may not be available in some browsers.

[url=http://peketec.de/trading/viewtopic.php?p=1633975#1633975 schrieb:marcovich schrieb am 22.10.2015, 17:31 Uhr[/url]"]Hi,

nachdem bereits Lynas wieder angesprungen ist in den letzten Tagen,

habe ich auch meine Position in Alkane Resources wieder aufgefüllt, zu ~0,24 A$

MCap ~ 100 Mio A$

Cash on Bank ~ 20 Mio A$

Cash Flow im Q3 10Mio A$

no debt

hier der Sept. Q3 Activity Report mit Zahlen und Beschreibung DZP: http://www.asx.com.au/asxpdf/20151016/pdf/4323plxvwkbxl9.pdf

DZP Projekt wird hoch interessant. Es ist trotz der aktuell äußerst niedrigen Rohstoffpreise sehr profitabel, sollte sich die Stimmung für Seltene Erden, Zirkonium, Hafnium uvm wieder aufhellen, dann steckt hier ein riesen Hebel drin, zudem ist es sehr vielseitig und mit der neuen Hafnium Separation auch nochmal interessanter geworden .. Demonstration Plant läuft seit fast 10 Jahren, wodurch die Separation stetig verbessert wurde. Haken: Allerdings sind erst die Facilities zu bauen für ~ 1,3 Mrd. Der nächste Schritt wird sein, eine Finanzierung hierfür auf die Beine zu stellen. Hier gefällt mir der Ansatz des Managements gut, ggf. Projekt Teilverkauf an strategischen Investor, Staatliche Kreditfinanzierung, Rest via KE bei gestiegenem Share Price.

Dann wird bei den aktuellen Preisen mit gerade aktualisierter Study mit folgenden Zahlen gerechnet:

Annual Revenues 580 Mio A$

EBITA 320 Mio A$

20 year NPV of 1,2 Mrd A$

Vielleicht für Euch interessant, freue mich falls es sich mal jemand anschaut, oder Meinungen dazu gibt

Geduld ist gefragt.

[url=http://peketec.de/trading/viewtopic.php?p=1633986#1633986 schrieb:PerseusLtd schrieb am 22.10.2015, 18:32 Uhr[/url]"]@fischländer: Hast du deine Pos. CMX noch ?

[url=http://peketec.de/trading/viewtopic.php?p=1634015#1634015 schrieb:Fischlaender schrieb am 22.10.2015, 21:13 Uhr[/url]"]Yep

[url=http://peketec.de/trading/viewtopic.php?p=1633986#1633986 schrieb:PerseusLtd schrieb am 22.10.2015, 18:32 Uhr[/url]"]@fischländer: Hast du deine Pos. CMX noch ?

[url=http://peketec.de/trading/viewtopic.php?p=1634016#1634016 schrieb:Fischlaender schrieb am 22.10.2015, 21:20 Uhr[/url]"]Grad gesehen warum du fragst, versteh den Anstieg nicht, hat ev. jemand unllimitiert gekauft, fundamental hat sich nix getan.

[url=http://peketec.de/trading/viewtopic.php?p=1634015#1634015 schrieb:Fischlaender schrieb am 22.10.2015, 21:13 Uhr[/url]"]Yep

[url=http://peketec.de/trading/viewtopic.php?p=1633986#1633986 schrieb:PerseusLtd schrieb am 22.10.2015, 18:32 Uhr[/url]"]@fischländer: Hast du deine Pos. CMX noch ?

[url=http://peketec.de/trading/viewtopic.php?p=1633386#1633386 schrieb:Rookie schrieb am 20.10.2015, 18:32 Uhr[/url]"]Ganfeng Increases Stake in Avalonia Lithium Project, Ireland and Finalizes Exploration Loan Agreement with International Lithium for Mariana Lithium Project, Argentina

http://internationallithium.com/ganfeng-increases-stake-in-avalonia-lithium-project-ireland-and-finalizes-exploration-loan-agreement-with-international-lithium-for-mariana-lithium-project-argentina/

[url=http://peketec.de/trading/viewtopic.php?p=1623649#1623649 schrieb:Rookie schrieb am 15.09.2015, 21:48 Uhr[/url]"]Lithium Brine

Dajin

» zur Grafik

International Lithium

» zur Grafik

Pure Energy

» zur Grafik

Lithium Hardrock

Nemaska

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1624448#1624448 schrieb:Kostolanys Erbe schrieb am 17.09.2015, 20:51 Uhr[/url]"]

Algold begins exploration at Kneivissat, Legouessi

2015-09-17 13:17 ET - News Release

Mr. Francois Auclair reports

ALGOLD RESOURCES LTD, COMPLETES REQUIREMENTS OF THE CARACAL EARN-IN AGREEMENT & PROVIDES UPDATE ON Q3 2015 EXPLORATION PROGRAM IN MAURITANIA

Algold Resources Ltd. has made progress on its third quarter 2015 exploration program in Mauritania, including work being carried out on both the Kneivissat and Legouessi properties.

During first quarter 2015, Algold completed its phase I exploration program on the Legouessi property, in accordance with the terms of the Caracal gold earn-in agreement, and, as a result, has earned its 51-per-cent participating interest in the Legouessi property. The interest in Legouessi will be held by a newly incorporated joint venture company, in which Algold will initially hold 51 per cent, with the balance held by Caracal. Under the terms of the agreement, Algold can increase its participation in the joint venture to 75 per cent and then 90 per cent, upon the completion of the phase II exploration program (for details, see press release dated Oct. 10, 2013).

In third quarter 2015, Algold initiated an extended field exploration program on both the Kneivissat and Legouessi properties, consisting of: a detailed IP (induced polarization) geophysical survey, detailed geological mapping, and limited trenching and sampling. In total, a 100-kilometre line survey will be carried out over the four main prospects: KC-LSO, NL, LC and SL (map details at Algold website). The principal objective of this exploration work is to delineate, with better accuracy, the chargeable units observed in the course of the 2014 IP survey and overlay them with the drilling results completed in second quarter 2014.

The results of the IP and mapping surveys will allow Algold to better estimate the size and orientation of the chargeable units, and target more efficiently the reverse circulation drilling program, anticipated to start in early Q1 2016.

Quality assurance/quality control (QA/QC)

Analytical work for soil geochemical samples and rock chip samples is carried out at the independent ALS Abilab Laboratories Ltd. in Bamako, Mali. Samples are stored at Algold's field camp and put into sealed bags until delivered by a geologist to the ALS preparation laboratory in Nouakchott, Mauritania. RC samples were combined to create two-metre composite samples. QA/QC procedures are followed, and 2 per cent gold standards, 2 per cent blanks and 2 per cent duplicates are added to the sample batch. Soil samples are sieved and prepared for shipping to Bamako. In Bamako, samples are crushed and pulverized to 200 mesh (80 microns), and a 30-gram split is analyzed by fire assay with an AA (atomic absorption) finish. ICP (inductively coupled plasma) analysis is conducted at the ALS Chemex Vancouver laboratory.

Blanks and duplicates are used to monitor laboratory performance during the analysis. Analytical work for the drilling program conducted by Caracal was carried out at the ALS Ireland laboratory under the supervision of a senior geologist.

This press release has been reviewed for accuracy and compliance under National Instrument 43-101 by Andre Ciesielski, DSc, PGeo, Algold Resources Ltd. lead consulting geologist and qualified person.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aALG-2311860&symbol=ALG®ion=C

[url=http://peketec.de/trading/viewtopic.php?p=1592577#1592577 schrieb:Kostolanys Erbe schrieb am 09.06.2015, 08:01 Uhr[/url]"]Algold Resources Ltd

Symbol C : ALG

Shares Issued 47,080,671

Close 2015-06-03 C$ 0.185

Recent Sedar Documents

View Original Document

Algold closes two private placements for $2.51-million

2015-06-04 11:27 ET - News Release

Mr. Benoit LaSalle reports

ALGOLD ANNOUNCES CLOSING OF A $2.5 MILLION PRIVATE PLACEMENT

Algold Resources Ltd. has closed its previously announced brokered private placement financing, conducted through a syndicate of agents led by Beacon Securities Ltd. and including Paradigm Capital Inc., of 7,319,772 units at a price of 22 cents per unit for gross proceeds to the corporation of $1,610,349.84. Concurrent with the brokered private placement, the corporation closed a non-brokered private placement of 4,102,152 units at a price of 22 cents per unit for additional gross proceeds to the corporation of approximately $902,473, and together with the brokered private placement, total gross proceeds to the corporation of approximately $2,512,823. Each unit consists of one common share of Algold and one share purchase warrant entitling the holder to subscribe for one share at a price of 30 cents for a period of 18 months from the closing date of the offering.

The corporation paid to the agents a cash commission of 7 per cent of the gross proceeds raised in connection with the brokered portion of the offering, and issued to the agents a number of compensation options equal to 7 per cent of the units issued in connection with the brokered portion of the offering, with each option entitling the agents to subscribe for one unit at a price of 22 cents for a period of 12 months from the closing date of the offering.

These securities were issued under applicable prospectus exemptions, and will be subject to a statutory hold period of four months and one day from closing of the placement.

Algold's chief executive officer, Francois Auclair, commented, "The announced financing will enable Algold to build on its existing exploration results, and to meet additional corporate objectives through the ongoing systematic exploration of our properties in Mauritania." Algold's chairman of the board, Benoit LaSalle, added, "Our ability to complete this financing under the current market conditions for gold exploration companies reflects a strong and ongoing commitment from both current and new investors to Algold's corporate objectives and its management team."

© 2015 Canjex Publishing Ltd. All rights reserved.

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aALG-2285794&symbol=ALG®ion=C

[url=http://peketec.de/trading/viewtopic.php?p=1588527#1588527 schrieb:Kostolanys Erbe schrieb am 22.05.2015, 00:55 Uhr[/url]"]Neuvorstellung & auf meiner Watchlist gelandet:

Algold Resources:

Algold Resources Ltd. – (TMX : ALG) is a mineral exploration company engaged in the acquisition, exploration and development of African mineral properties. ALG is a publicly traded company listed TSX Venture Exchange. The company has recently acquired:

Two valuable properties in close proximity of the Tasiast mine in Mauritania,

Two strategic properties in Burkina Faso,

http://algold.com/

Bekommen in dieser Marktphase schnell mal $$$

Algold Announces Up to $3 Million Overnight Marketed Private Placement Financing

MONTREAL, May 13, 2015 /CNW/ - Algold Resources Limited (ALG: TSXV – the "Corporation" or "Algold") www.algold.com is pleased to announce that it has appointed a syndicate of agents (the "Agents") led by Beacon Securities Limited and including Paradigm Capital Inc. as its agents to sell, by private placement on an overnight marketed basis, units (the "Units") of Algold at a price (the "Issue Price") to be determined in the context of the market for gross proceeds of up to approximately CDN$3,000,000 (the "Offering"). Each Unit will be comprised of one common share (a "Common Share") in the capital of the Corporation and one common share purchase warrant, each entitling the holder thereof to acquire a Common Share at a price to be determined in the context of the market for a period of 18 months from the closing of the Offering.

The net proceeds from the Offering are intended to be used to advance the Kneivissat and Legouessi properties for working capital and general corporate purposes.

The Company has agreed to pay the Agents a cash fee equal to 7.0% of the gross proceeds from the Offering. As additional compensation, the Agents will be issued compensation options entitling the Agents to purchase that number of Common Shares equal to 7.0% of the number of Units sold under the Offering exercisable at Issue Price for a period of 12 months from the closing date of the offering.

The closing of this equity offering is expected to occur on or the week of May 25, 2015 and is subject to receipt of all necessary regulatory approvals. The Units, including all underlying securities thereof, and the compensation options issued with respect to the Offering will be subject to a four month hold period in accordance with applicable Canadian securities laws.

This news release does not constitute an offer of securities for sale in the United States. The securities being offered have not been, nor will they be, registered under the United States Securities Act of 1933, as amended, and such securities may not be offered or sold within the United States absent U.S. registration or an applicable exemption from U.S. registration requirements.

ABOUT ALGOLD

Algold Resources Ltd is focused on the exploration and development of gold deposits in West Africa. The board of directors and management team are seasoned resource industry professionals with extensive experience in the exploration and development of world-class gold projects in Africa.

Algold is the operator on both the Kneivissat and Legouessi Properties. The Kneivissat property is 90% owned by Algold and the Legouessi property is being managed through a 51% earn-in interest agreement with Caracal (Electrum Group Companies). Algold can earn up to a 90% interest in the Legouessi exploration permit (see October 10, 2013 press release for more details), however, Caracal has the right to participate in the joint venture at either 51% or 75%, by funding its share of expenditures.

http://app.quotemedia.com/quotetools/newsStoryPopup.go?storyId=75471293&topic=ALG:CA&symbology=tmx&cp=null&webmasterId=101341

Aktuelle Präsentation:

http://algold.com/wp-content/uploads/2015/05/Presentation-Algold.pdf

Hauptgrund für die Watchlist ist der Typ

Mr. La Salle is the President and CEO of Windiga Energy, a company involved in renewable resource development in Africa. He is also founder of SEMAFO (a TSX-listed company), and a well-known mining entrepreneur in Canada and Africa. Mr. La Salle grew SEMAFO from junior explorer to a +250,000 ounces per year gold producer in West Africa (3 mines). Mr. La Salle is the Chairman of Sama Resources exploring for Nickel in Cote d’Ivoire, and Chairman of Canadian Council on Africa. M La Salla was co-founder in 1980 and a partner until 2004 of Grou, La Salle & Associates CA (“GLA”), based in Montreal (Quebec), an accounting firm offering audit and accounting services, with a strong emphasis on financial and corporate reorganization and the implementation of international corporate structures. The firm grew from two original partners to a staff of over 50.

» zur Grafik

» zur Grafik

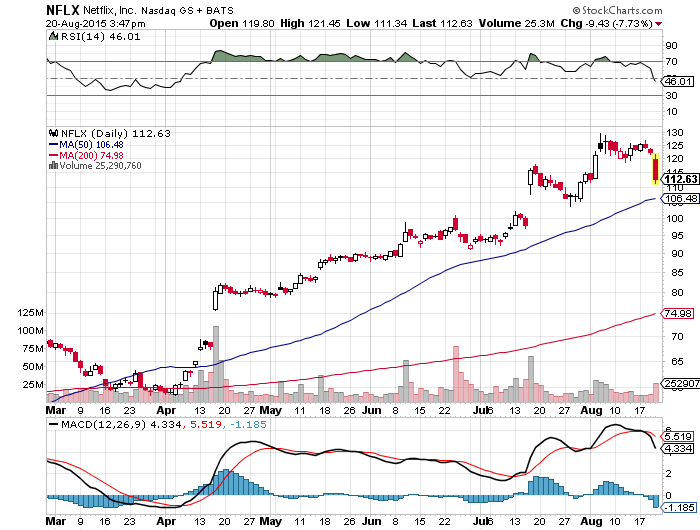

[url=http://peketec.de/trading/viewtopic.php?p=1632896#1632896 schrieb:Kostolanys Erbe schrieb am 16.10.2015, 21:08 Uhr[/url]"]NFLX nach den Zahlen...

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1631878#1631878 schrieb:Kostolanys Erbe schrieb am 13.10.2015, 22:41 Uhr[/url]"]Nee doch nicht, erstm al hat NFLX das Island-Gap geschlossen... somit keine weiteren Gaps oben zu schliessen

» zur Grafik

Infinera ...auf zum Gap-Close...

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1628175#1628175 schrieb:Kostolanys Erbe schrieb am 29.09.2015, 20:59 Uhr[/url]"]Anscheinend ist der Deckel erst mal nach oben die 100 $ Marke...

» zur Grafik

Infinera an einer wichtigen horizontalen Unterstützungslinie:

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1622038#1622038 schrieb:Kostolanys Erbe schrieb am 09.09.2015, 17:48 Uhr[/url]"]Ein anderer Wert neben NFLX, wo sich charttechnisch eine S-K-S Formation bildet ist INFN und hat um die 14 US-Dollar noch ein Gap zu schliessen!

]» zur Grafik

Sept 9, 2015

Netflix readies for launch in Hong Kong, other Asian markets

Netflix shares jump more than 6% on news of Asia Expansion

http://www.marketwatch.com/story/netflix-readies-for-launch-in-hong-kong-other-asian-markets-2015-09-09?siteid=bigcharts&dist=bigcharts

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1619399#1619399 schrieb:Kostolanys Erbe schrieb am 31.08.2015, 20:51 Uhr[/url]"]Montag, 31.08.2015 - 17:52 Uhr

NETFLIX - Das Gap ruft

http://www.godmode-trader.de/analyse/netflix-das-gap-ruft,4323140

[/quote[url=http://peketec.de/trading/viewtopic.php?p=1618671#1618671 schrieb:Kostolanys Erbe schrieb am 27.08.2015, 23:28 Uhr[/url]"]Scheinchen CW2T7E klebt wieder am Lapi...

NFLX könnte charttechnisch um die 117-120 US$ die rechte Schulter einer SKS Formation ausbilden....?! Beobachten !!!

» zur Grafik

CEO hat schnell noch mal schön abgesahnt und seine Aktienoptionen versilbert...

und hält aktuell nicht mal eine Aktie seines Unternehmens !!!Ganz schön traurig... Wieviel Optionen er noch einlösen kann, weiss ich nicht...

» zur Grafik

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1617276#1617276 schrieb:Kostolanys Erbe schrieb am 24.08.2015, 21:16 Uhr[/url]"]@Olli

[url=http://peketec.de/trading/viewtopic.php?p=1616804#1616804 schrieb:Ollinho schrieb am 24.08.2015, 10:24 Uhr[/url]"]GW Kosto!!

[url=http://peketec.de/trading/viewtopic.php?p=1616774#1616774 schrieb:Kostolanys Erbe schrieb am 24.08.2015, 09:40 Uhr[/url]"]Verkauf zu 0,92 € !!!")

Börse heisst spekulieren und auch mal Gewinne mitnehmen!

Bin heute Abend mal auf die letzte Handelsstunde in USA gespannt...

[url=http://peketec.de/trading/viewtopic.php?p=1616461#1616461 schrieb:Kostolanys Erbe schrieb am 21.08.2015, 21:30 Uhr[/url]"]Danke @Olli

Scheinchen aktuell bei 0,72 €

https://www.boerse-stuttgart.de/de/boersenportal/wertpapiere-und-maerkte/hebelprodukte/optionsscheine/factsheet/?ID_NOTATION=137310115

NFLX aktuell die 50-Tage-Linie nach unten durchbrochen

Immer noch viel Speck drauf...

Und so langsam werden die die auf Margin debts zocken

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1616040#1616040 schrieb:Ollinho schrieb am 20.08.2015, 22:22 Uhr[/url]"]Sauber Kosto!!!

[url=http://peketec.de/trading/viewtopic.php?p=1616023#1616023 schrieb:Kostolanys Erbe schrieb am 20.08.2015, 21:50 Uhr[/url]"]

200-Tage-Linie bei ca. 75 $ !!!

Scheinchen steht aktuell bei 0,57 €

https://www.boerse-stuttgart.de/de/boersenportal/wertpapiere-und-maerkte/hebelprodukte/optionsscheine/factsheet/?ID_NOTATION=137310115

» zur Grafik

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1615368#1615368 schrieb:Kostolanys Erbe schrieb am 19.08.2015, 11:01 Uhr[/url]"]Kleine Put Speku-Posi CW2T7E zu 0,43€ genommen.

[url=http://peketec.de/trading/viewtopic.php?p=1615208#1615208 schrieb:Kostolanys Erbe schrieb am 18.08.2015, 22:40 Uhr[/url]"]Mich reizt ja irgendwie als Gapi-Freak ein Put (normalen OS / Kein Knock-out-Scheinchen in dieser Situation); Bewertung ist echt krass, irgendwann werden auch mal die von NFLX evtl. ein Quartal enttäuschen

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1634978#1634978 schrieb:Rookie schrieb am 27.10.2015, 17:33 Uhr[/url]"]Andere Meinung zu Red Eagle

Red Eagle Mining Has Huge Upside Potential, But Carries Too Much Risk

Red Eagle Mining owns an attractive gold development project in Colombia called Santa Rosa.

A feasibility study released on the project was positive, with a net present value of $104 million and a rate of return of 53%.

Still, Red Eagle carries numerous risks that makes the stock a little too risky as an investment.

Red Eagle Mining (OTCQX:RDEMF) is a junior gold company that owns the Santa Rosa gold project in Colombia. This project is fully permitted and is fully funded to initial production, which is expected to begin in 2016. However, I personally feel that Red Eagle carries a little too much risk for an investment currently, and I'll explain my thoughts below.

First, an overview of Red Eagle's 100%-owned Santa Rosa project. This project contains 405,000 ounces of gold reserves at 5.2 g/t, and a feasibility study outlines a 1,000 tonne per day operation, with expected annual production of 50,000 gold ounces over an eight year mine life.

Initial capital costs are just $74 million, and the mine is estimated to produce gold at cash costs of just $596 per ounce (with all-in sustaining costs estimated at $763 per ounce). This means at $1,200 gold, margins would be $437 per ounce, and with 50,000 ounces of gold produced annually, annual EBITDA would be $21.8 million.However, you'll see in the feasibility study that at $1,100 gold, the post-tax net present value of this project actually drops quite a bit, to just over $50 million. That's basically what the company is currently valued at ($40.10 million market cap), leaving virtually zero room for error. Only at $1,300 gold and above do things get interesting, with the net present value jumping to $100+ million at $1,300 gold and $160+ million at $1,500 gold.

I'd argue that gold prices would need to be at $1,500 gold for this stock to be attractive at its current valuation, given the numerous risks associated with developing and advancing a gold deposit to production.As mentioned, the project requires $74 million in initial capital, which seems like a big amount given the size of Red Eagle. However, the company actually raised $60 million via a construction facility with Orion Finance in April of 2015 and a $19.35 million equity financing on August 21, so the project is technically fully funded to production - which is a major accomplishment by Red Eagle, to be fair.

As for the equity financing, Red Eagle had to issue 71.67 million common shares at a price of C$.27 per share, diluting existing shareholders by more than 50%.

While I thought the equity financing was still positive news, as it was done at a fair price, the construction facility is pretty risky in my opinion. While Red Eagle doesn't have to pay principal or interest for up to 18 months following its first advance, the facility comes with a five year term and advances under the facility bear interest at LIBOR + 7.5%, which is quite expensive.

In addition, a production payment of $30 per ounce produced is payable on the first 405,000 ounces of gold produced at the mine, and Red Eagle had to grant 5 million warrants to Orion. All amounts outstanding under the credit facility are secured by Red Eagle's property and assets.

For this reason, issuing debt to advance a gold mine to production is really risky, as many, many things can go wrong in the process. Just take a look at Rubicon Minerals (NYSEMKT:RBY), which recently had to temporarily suspend mill operations at its Phoenix Gold project, Midway Gold (NYSEMKT:MDW), which filed for bankruptcy after messing up its resource estimate and breaking convenents on its project finance facility, and Colossus Minerals, which went over budget and ran out of money while developing its Serra Pelada project. There are just many, many risks in this business.

The bottom line: Red Eagle's Santa Rosa project carries attractive economics based on its feasibility study, and looks like it holds considerable exploration upside, but I don't feel investors being compensated for these risks at the current share price. I'd recommend avoiding shares.

[url=http://peketec.de/trading/viewtopic.php?p=1634980#1634980 schrieb:PerseusLtd schrieb am 27.10.2015, 17:37 Uhr[/url]"]Hab ich heute bereits gelesen , lächerlich

[url=http://peketec.de/trading/viewtopic.php?p=1634978#1634978 schrieb:Rookie schrieb am 27.10.2015, 17:33 Uhr[/url]"]Andere Meinung zu Red Eagle

Red Eagle Mining Has Huge Upside Potential, But Carries Too Much Risk

[url=http://peketec.de/trading/viewtopic.php?p=1622795#1622795 schrieb:Fischlaender schrieb am 11.09.2015, 15:00 Uhr[/url]"]Die sprachen von 1,8 USD, da sind wir laengst drunter...

[url=http://peketec.de/trading/viewtopic.php?p=1622785#1622785 schrieb:greenhorn schrieb am 11.09.2015, 15:45 Uhr[/url]"]YRI - das es so weit geht hätte ich nicht gedacht, aber die 1,80 CAD sind in Reichweite, werde dort zukaufen

[url=http://peketec.de/trading/viewtopic.php?p=1610064#1610064 schrieb:greenhorn schrieb am 31.07.2015, 09:32 Uhr[/url]"]SK gestern bei 2,38 CAD........siehe Analys unten, hätte getrost warten sollen, läuft eventuelle noch bis 1,81 CAD runter

für mich trotzdem sehr positive Entwicklung

Schuldenreduktion um 129 Mio $

Cashbestand 119 Mio $

All-in sustaining costs per ounce bei unter 900$ !

Zahlen Dividende

July 30, 2015 16:40 ET

Yamana Gold Announces Second Quarter 2015 Results

Focus remains on operational execution with production on track to meet expectations

http://www.marketwired.com/press-re...cond-quarter-2015-results-tsx-yri-2043792.htm

TORONTO, ONTARIO--(Marketwired - July 30, 2015) - YAMANA GOLD INC. (TSX:YRI)(NYSE:AUY) ("Yamana" or "the Company") is herein reporting its financial and operating results for the second quarter 2015, with some highlights provided as follows.

•Total gold production of 298,818 ounces representing a 7% increase in gold production from continuing operations compared to the second quarter of 2014; including

◦9% increase in gold production at core operations(1) compared to the second quarter of 2014.

◦Total gold production of approximately 604,000 ounces to mid-year.

•By-product all-in sustaining costs ("AISC")(2,3) of $896 per ounce of gold; including

◦$763 per ounce of gold at core operations.

•Production of 2.4 million ounces of silver at by-product AISC(2,3) of $10.72 per ounce.

◦Total silver production of approximately 4.9 million ounces to mid-year.

•33.6 million pounds of copper production at cash costs(2) of $1.39 per pound, representing a 21% decrease in cash costs compared to the second quarter of 2014.

◦Total copper production of approximately 60.5 million pounds to mid-year.

•Cash flows(2,4,5) from continuing operations before changes in non-cash working capital of $149.3 million or $0.16 per share; representing

◦56% increase compared to the first quarter of 2015; and

◦$0.33 of operating cash flows before changes in non-cash working capital per dollar of revenue generated in the second quarter, an increase of 57% from the first quarter of 2015.

•Cash flows from continuing operations after changes in non-cash working capital(5) for the second quarter of $123.4million or $0.13 per share.

•A $4.6 million or 13% decrease in general and administrative expense compared to the second quarter of 2014.

•Adjusted loss from continuing operations(2) of $8.3 million or $0.01 per share; and

◦Net loss from continuing operations of $7.0 million or $0.01 per basic share.

(All amounts are expressed in United States dollars unless otherwise indicated.)

1.Core operations includes Chapada, El Peñón, Gualcamayo, Canadian Malartic, Mercedes, Minera Florida and Jacobina.

2.Refers to a non-GAAP measure. Reconciliation of non-GAAP measures are available at www.yamana.com/Q22015

3.Includes cash costs, sustaining capital, corporate general and administrative expense and exploration expense.

4.Excluding cash distributions from Alumbrera.

5.Cash flows from operating activities.

The Company continues to focus on operational execution and remains on track to meet total 2015 production guidance. In the first half of 2015, the Company produced approximately 47% of expected full year gold production with the majority of its portfolio tracking at or above budget expectations. In addition, both silver and copper production were tracking to approximately 50% of expected full year production by mid-year. As in previous years, the Company expects production growth and cost reductions in the second half, most notably with the largest quarterly contribution expected in the fourth quarter. Within the Company's seven core assets, Jacobina and Mercedes are expected to deliver the most significant production improvements in the second half of 2015, along with increases in production at Gualcamayo, Chapada and Canadian Malartic.

During the quarter, the Company continued to focus on maintaining a stable financial position and improving its overall debt levels by triggering an early conversion of its convertible unsecured subordinated debentures assumed on the acquisition of Canadian Malartic. The Company used shares and cash which had been set aside upon completion of the acquisition to contribute to a reduction in the Canadian Malartic debt by $51 million. The Company is positioned to further advance its debt repayment plans with the planned disposition of some non-core assets and the going public event for Brio Gold Inc. ("Brio Gold"), a subsidiary of the Company. Further reductions to general and administrative expenses and other cost savings will also contribute to future debt reductions.

In the first half of the year, net debt was reduced by $129 million summarized as follows:

[url=http://peketec.de/trading/viewtopic.php?p=1605769#1605769 schrieb:greenhorn schrieb am 21.07.2015, 17:06 Uhr[/url]"]mach nun trotzdem die 2.Posi zu 2,83 CAD - MischEK bei 3,40 CAD

[url=http://peketec.de/trading/viewtopic.php?p=1602174#1602174 schrieb:greenhorn schrieb am 09.07.2015, 09:22 Uhr[/url]"]

"....Seit Mai hat sich neben der übergeordnet bärischen Gesamtsituation ein kurzfristiger Abwärtstrend gebildet, welcher durchaus wegweisend sein könnte. Sollte die Aktie daher weiter zurückfallen, so wäre insbesondere unterhalb von 2,64 USD eine weitere Zuspitzung der Verlustserie bis 2,00 USD und darunter bis 1,81 USD zu erwarten. Die Stimmung rund um die Aktie bliebe dementsprechend weiter negativ, sodass man auf den Beginn einer nachhaltigen Bodenbildung weiter warten müsste..."

http://www.rohstoff-welt.de/news/artikel.php?sid=54773#Yamana-Gold-bleibt-ein-Trauerspiel

[url=http://peketec.de/trading/viewtopic.php?p=1594075#1594075 schrieb:Kostolanys Erbe schrieb am 12.06.2015, 09:48 Uhr[/url]"]Gestern 103.500 shares Insiderkäufe!

[url=http://peketec.de/trading/viewtopic.php?p=1594020#1594020 schrieb:greenhorn schrieb am 12.06.2015, 08:39 Uhr[/url]"]ja, so ist zumindest meine Denke gewesen!

[url=http://peketec.de/trading/viewtopic.php?p=1593940#1593940 schrieb:Kostolanys Erbe schrieb am 12.06.2015, 00:03 Uhr[/url]"]Evtl. doppelter Boden aus November 2014

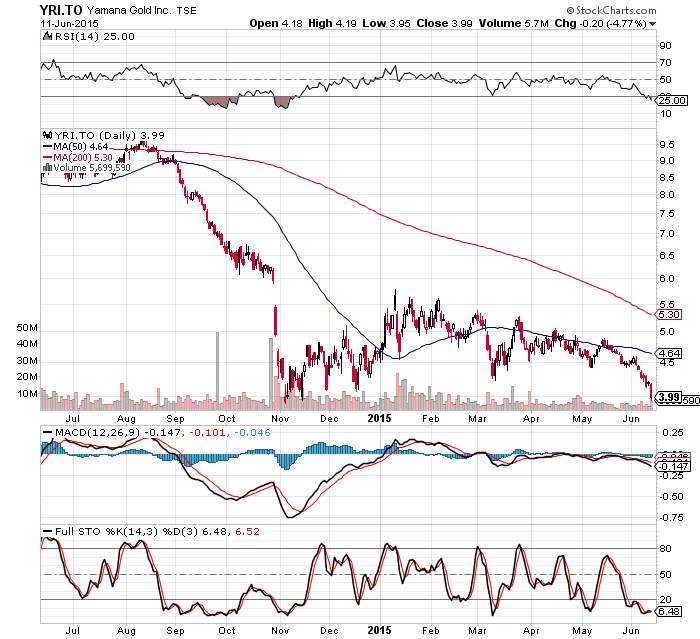

RSI jetzt im überverkauften Bereich!

» zur Grafik

[url=http://peketec.de/trading/viewtopic.php?p=1593873#1593873 schrieb:greenhorn schrieb am 11.06.2015, 17:03 Uhr[/url]"]YRI mal ne 1. Posi Long zu 3,95/3,97 CAD - um 2,86 Euro

Wir verwenden Cookies, die für das Funktionieren dieser Website unerlässlich sind, und optionale Cookies, um Ihr Erlebnis zu verbessern.

Lese weitere Informationen und konfiguriere deine Einstellungen

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}