Kostolanys Erbe schrieb am 10.12.2015, 21:33 Uhr[/url]"]Zuletzt ging es bei Altius auch ordentlich abwärts...

tax-selling season

")

Altius Minerals loses $1.14-million in fiscal Q2

2015-12-10 09:06 ET - News Release

Mr. Ben Lewis reports

ALTIUS MINERALS CORPORATION REPORTS QUARTERLY ATTRIBUTABLE REVENUE OF $8,534,000 AND ADJUSTED EBITDA OF $6,729,000

Altius Minerals Corp. had attributable revenue of $8,534,000, adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) of $6,729,000 and a net loss of $1.14-million or three cents per share for the quarter ended Oct. 31, 2015, compared with attributable revenue of $7,027,000, adjusted EBITDA of $7,693,000 and a net loss of $25,348,000 for same period last year. Year to date, the corporation has attributable revenue of $18,319,000, adjusted EBITDA of $13,868,000 and net loss of $1,682,000.

The current-period results were positively affected by royalty revenues from Altius's newly acquired 777 royalty of $2,361,000 as well as Prairie Royalties and Voisey's Bay of $5,077,000 and $372,000, respectively. Revenues were offset by non-cash charges such as amortization of royalty interests of $1,829,000 and equity losses of $1,002,000 and impairment losses of $1,695,000 in the corporation's investment in Alderon.

SUMMARY OF THE FINANCIAL RESULTS

For the three months ended For the six months ended

Oct. 31, Oct. 31,

2015 2014 2015 2014

Royalty revenue

777 $2,361,000 - $4,892,000 -

Coal 3,819,000 4,558,000 8,072,000 9,516,000

Potash 1,258,000 1,344,000 2,760,000 2,418,000

Voisey's Bay 372,000 683,000 1,049,000 1,262,000

CDP 406,000 355,000 862,000 859,000

Interest and investment 316,000 68,000 682,000 149,000

Other 2,000 19,000 2,000 40,000

Attributable revenue 8,534,000 7,027,000 18,319,000 14,244,000

Adjusted EBITDA 6,727,000 7,693,000 13,868,000 7,693,000

Net (loss) attributable

to common shareholders (1,140,000) (25,348,000) (1,682,000) (25,348,000)

Net (loss) per share

basic and diluted (0.03) (0.77) (0.04) (0.77)

Total assets 448,546,000 394,267,000 448,546,000 394,267,000

Total liabilities 96,827,000 130,471,000 96,827,000 130,471,000

Cash dividends declared

and paid to shareholders 1,198,000 nil 2,396,000 nil

http://www.stockwatch.com/News/Item.aspx?bid=Z-C%3aALS-2333505&symbol=ALS®ion=C

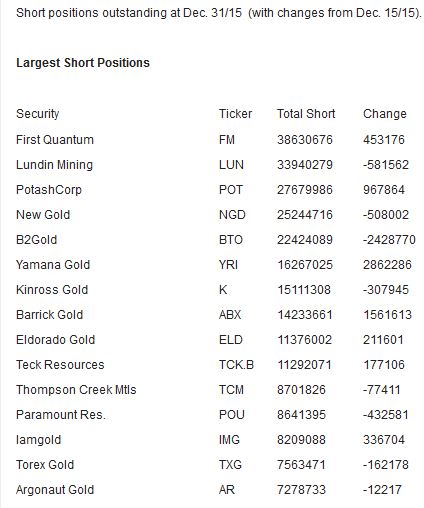

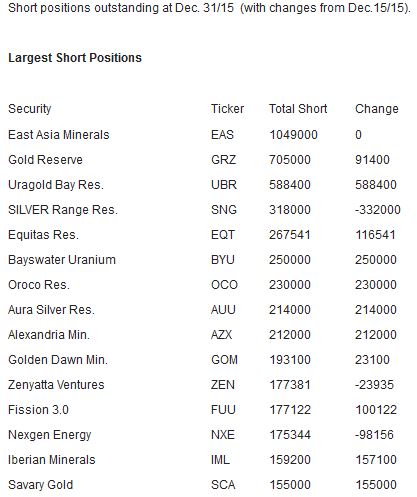

» zur Grafik